Florida’s home insurance market is facing an unprecedented crisis, characterized by skyrocketing premiums, limited availability, and a volatile real estate landscape. This escalating situation impacts not only homeowners but also the state’s economy, forcing a critical examination of the underlying causes and potential solutions. The confluence of factors – from increasingly frequent and severe hurricanes to a complex legal environment – has created a perfect storm, leaving many Floridians struggling to afford adequate coverage.

This exploration delves into the multifaceted nature of the crisis, examining the key drivers of rising costs, the impact on homeowners and the real estate market, the responses of insurance companies and the government, and ultimately, the potential long-term consequences for the state. We will analyze the interplay between natural disasters, litigation, regulatory frameworks, and economic pressures, providing a comprehensive overview of this critical issue.

The Rising Costs of Home Insurance in Florida

Florida’s home insurance market has experienced a dramatic upheaval in recent years, leaving many homeowners struggling with significantly increased premiums. This surge in costs is a complex issue stemming from a confluence of factors, impacting affordability and accessibility for a large segment of the population.

Factors Contributing to Increased Premiums

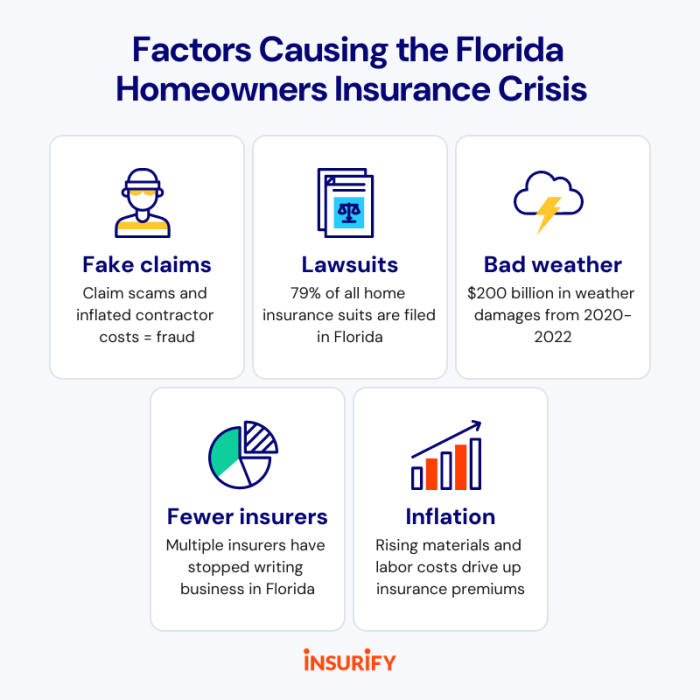

Several interconnected factors have driven the substantial increase in Florida home insurance premiums over the past five years. These include a rise in the frequency and severity of hurricane-related claims, increased litigation costs associated with insurance disputes, and the financial instability of some insurance companies operating within the state. Reinsurance costs, which help insurers cover catastrophic losses, have also skyrocketed, further impacting premiums. Additionally, the increasing cost of construction materials and labor has inflated the cost of repairing or rebuilding damaged properties, leading insurers to raise premiums to offset these expenses. Fraudulent claims also contribute significantly to the problem, adding to the overall financial burden on insurers.

Average Cost Increases by Region

Precise regional breakdowns of average cost increases require access to real-time insurance data which fluctuates constantly. However, it’s generally accepted that coastal areas, particularly those highly vulnerable to hurricanes, have experienced the most significant premium increases. Areas like South Florida (Miami-Dade, Broward, Palm Beach counties) and the panhandle have seen particularly steep rises, while more inland regions have seen increases, albeit generally less dramatic. The lack of consistent, publicly available data across all regions makes precise quantification difficult.

Percentage of Homeowners Facing Unaffordable Premiums

Determining the exact percentage of Florida homeowners facing unaffordable premiums is challenging due to the lack of comprehensive, publicly accessible data. However, anecdotal evidence and reports from consumer advocacy groups suggest a substantial portion of the population is struggling. Many homeowners are finding themselves forced to choose between paying exorbitant premiums or foregoing coverage altogether, leaving them vulnerable in the event of a disaster. This situation disproportionately affects lower-income homeowners and those living in vulnerable coastal communities.

Comparison of Florida Premium Costs to Other States

| State | Average Annual Premium (Estimate) | Hurricane Risk | Litigation Environment |

|---|---|---|---|

| Florida | $4,000 – $6,000+ (highly variable) | High | Highly litigious |

| Texas | $1,500 – $3,000 | Moderate | Moderately litigious |

| Louisiana | $2,000 – $4,000 | High | Highly litigious |

| South Carolina | $1,000 – $2,500 | Moderate | Moderately litigious |

*Note: These are estimated average annual premiums and can vary significantly based on coverage, location, and other factors. Actual costs may differ considerably. The data presented reflects a general comparison and should not be considered definitive. Detailed, up-to-date information should be obtained from individual insurance providers.

Impact on Homeowners and the Real Estate Market

The soaring cost of home insurance in Florida is significantly impacting homeowners and the state’s real estate market, creating a ripple effect felt across various socioeconomic groups and aspects of the housing landscape. The consequences extend beyond simple financial strain, affecting property values, sales, and the overall affordability of housing in the Sunshine State.

The escalating premiums are placing a considerable financial burden on Florida homeowners. Many are forced to choose between paying exorbitant insurance costs or facing potential foreclosure. This financial strain is particularly acute for those with fixed incomes, such as retirees, and low-to-moderate income families who already struggle to afford basic necessities. The increased insurance burden often forces difficult choices, potentially impacting access to healthcare, food security, and other essential aspects of daily life.

Financial Strain and Potential Displacement of Homeowners

The dramatic increase in home insurance premiums is pushing many Floridians to the brink of financial hardship. For example, a homeowner who previously paid $2,000 annually might now face a bill of $5,000 or more, a 150% increase. This unexpected and substantial increase can deplete savings, necessitate taking on additional debt, or even lead to the loss of a home through foreclosure. This financial strain disproportionately affects low-income families and seniors on fixed incomes, leaving them vulnerable to displacement and homelessness. The inability to afford insurance premiums is becoming a major driver of home sales, as homeowners are forced to sell their properties to avoid further financial ruin.

Socioeconomic Disparities in the Impact of Rising Insurance Costs

The impact of the insurance crisis is not uniform across all socioeconomic groups in Florida. Low-income communities and those residing in areas deemed high-risk are disproportionately affected. These communities often have fewer resources to cope with the sudden increase in premiums and are more likely to experience financial distress and displacement. Conversely, higher-income homeowners, who might have greater financial reserves, can absorb the increased costs more easily. This disparity exacerbates existing inequalities in housing affordability and access.

Influence on Florida’s Real Estate Market

The rising cost of home insurance is significantly impacting Florida’s real estate market. Higher insurance premiums are directly reducing the affordability of homes, making it more difficult for potential buyers to enter the market. This reduced demand can lead to a decrease in property values, particularly in areas with high insurance costs. Furthermore, the uncertainty surrounding future insurance rates is creating hesitation among both buyers and sellers, slowing down the overall market activity. In some instances, properties are remaining unsold or selling at prices below their assessed value, due to the added financial burden of insurance.

Impact on Property Taxes and Affordability

The insurance crisis indirectly affects property taxes and overall housing affordability. As property values potentially decrease due to the high insurance costs, the assessed value of properties might also decline, resulting in lower property tax revenue for local governments. However, the cost of home insurance itself becomes a significant factor in the overall cost of homeownership, making housing less affordable for a larger segment of the population. This can lead to a decline in property values and potentially impact local government services reliant on property tax revenue. The interplay between insurance costs, property values, and property taxes creates a complex and challenging situation for homeowners and local governments alike.

The Future of Home Insurance in Florida

The current crisis in Florida’s home insurance market presents a complex web of challenges, but also potential opportunities for innovation and systemic reform. The long-term consequences will significantly impact homeowners, the real estate market, and the state’s economy, demanding proactive solutions from insurers, regulators, and lawmakers. Understanding the potential future scenarios is crucial for navigating this turbulent period.

Long-Term Consequences of the Crisis

The ongoing crisis risks creating a two-tiered system where only wealthier homeowners can afford adequate coverage, leaving many vulnerable to financial ruin in the event of a catastrophic event. This could lead to decreased property values in certain areas, impacting the overall health of the Florida real estate market. Increased litigation costs, coupled with the high frequency of severe weather events, are unsustainable in the current model. The exodus of insurers from the state also poses a threat to economic stability, potentially affecting construction, employment, and tourism. A prolonged crisis could lead to a significant reduction in available insurance options, forcing many homeowners to become self-insured, a risky proposition given the state’s vulnerability to hurricanes.

Challenges and Opportunities for Stakeholders

Insurers face the challenge of balancing profitability with social responsibility, requiring innovative risk assessment models and pricing strategies that account for climate change and evolving litigation landscapes. Regulators need to create a more stable and predictable regulatory environment that encourages insurers to remain in the market while protecting consumers. Homeowners need to actively engage in mitigation strategies, such as strengthening their homes and purchasing supplemental coverage, to reduce their risk profiles. The opportunity lies in fostering collaboration among all stakeholders to develop a sustainable, resilient, and equitable insurance market. This includes exploring alternative risk transfer mechanisms and leveraging technology to improve efficiency and transparency.

Potential for Innovation and Technological Solutions

Technological advancements offer several pathways to address the crisis. Advanced modeling techniques, incorporating climate data and building characteristics, can create more accurate risk assessments, leading to fairer and more transparent pricing. Blockchain technology can streamline claims processing and reduce fraud. Telematics and IoT devices can monitor homes for potential risks, enabling proactive mitigation and reducing claims. The development of parametric insurance products, which pay out based on pre-defined triggers (like wind speed), could simplify claims processing and expedite payouts. For example, a system could automatically assess damage based on satellite imagery following a hurricane, triggering a payout based on predetermined parameters.

A Potential Future Scenario for the Florida Home Insurance Market

One possible future scenario involves a hybrid model. A state-backed insurer of last resort could provide basic coverage to homeowners who struggle to find private insurance, similar to the model used in some other states. Simultaneously, private insurers would compete to offer a wider range of more comprehensive policies, using advanced risk modeling and technology to create more accurate pricing and efficient claims processing. This could result in higher premiums for some homeowners, particularly those in high-risk areas, but with greater access to coverage options and potentially faster claim settlements. Consumer experiences would vary based on location and risk profile, with those in lower-risk areas potentially benefiting from more competitive pricing. For example, homeowners in areas with robust building codes and mitigation measures might see lower premiums, while those in coastal areas might face higher premiums but with access to more comprehensive coverage options. This scenario requires a significant investment in technology and a collaborative approach from all stakeholders.

Wrap-Up

The Florida home insurance crisis presents a formidable challenge demanding innovative and collaborative solutions. While the immediate concerns revolve around affordability and availability, the long-term implications extend to the stability of the state’s real estate market and the overall economic well-being of its residents. Addressing this crisis requires a multi-pronged approach involving insurers, legislators, and homeowners alike, fostering a sustainable and equitable insurance market for the future. Only through comprehensive reform and proactive measures can Florida hope to mitigate the ongoing impact and build resilience against future challenges.

Questions Often Asked

What are the main reasons for the increase in homeowners insurance rates in Florida?

Increased hurricane frequency and severity, higher litigation costs, and increased reinsurance costs are the primary drivers.

Are there any government programs available to help Floridians afford home insurance?

Some state and local programs offer assistance, but availability and eligibility vary. It’s best to check with your local government or insurance agencies for specific programs.

What can homeowners do to lower their insurance premiums?

Homeowners can mitigate risk by reinforcing their homes to hurricane standards, exploring discounts offered by insurers, and shopping around for competitive rates.

How does the Florida home insurance crisis affect the state’s economy?

The crisis impacts the real estate market, potentially decreasing property values and hindering sales. It also impacts the financial stability of insurance companies and could affect the overall economic health of the state.