Choosing the right life insurance policy is a crucial step in securing your family’s financial future. It’s not just about protection; it’s about strategically planning for unforeseen circumstances and ensuring your loved ones are provided for. This comprehensive guide delves into the intricacies of selecting the “best” life insurance policy, considering your unique financial situation and long-term goals.

We’ll explore various policy types, from term life insurance’s affordability to the long-term growth potential of whole life policies. Understanding your needs, comparing providers, and navigating policy features are key elements we’ll dissect to empower you in making an informed decision. The process might seem daunting, but with the right knowledge, finding the perfect fit becomes achievable.

Defining “Best” Life Insurance

Finding the “best” life insurance policy isn’t about choosing a single, universally superior option. Instead, it’s about identifying the policy that most effectively aligns with your individual circumstances, financial goals, and risk tolerance. Several key factors influence this determination, making the process highly personalized.

The ideal life insurance policy depends on a multitude of factors, including your age, health, income, family responsibilities, and financial objectives. For example, a young, healthy individual with a growing family might prioritize a high coverage amount at a relatively low cost, while a retired individual with a significant net worth might focus on policies that offer tax advantages or legacy planning capabilities. Understanding these individual needs is paramount in selecting the appropriate coverage.

Life Insurance Policy Types and Their Suitability

Different types of life insurance policies offer varying levels of coverage, cost structures, and benefits. Matching the policy type to your specific needs is crucial for maximizing its effectiveness. The most common types include term life, whole life, universal life, and variable universal life insurance.

Comparison of Common Life Insurance Policy Types

Understanding the nuances between different policy types requires careful consideration of their features. The following table provides a comparison of key characteristics:

| Policy Type | Cost | Coverage | Benefits | Suitability |

|---|---|---|---|---|

| Term Life | Relatively low premiums | Coverage for a specific period (term) | Pure death benefit; affordable coverage for a set period | Individuals needing temporary coverage, those on a budget |

| Whole Life | Higher premiums than term life | Lifetime coverage | Death benefit, cash value accumulation (grows tax-deferred), potential loan options | Individuals seeking lifetime coverage and cash value growth |

| Universal Life | Flexible premiums, adjustable death benefit | Lifetime coverage | Death benefit, cash value accumulation (growth depends on market performance and interest rates), flexible premium payments | Individuals wanting flexibility in premium payments and death benefit adjustments |

| Variable Universal Life | Flexible premiums, adjustable death benefit, investment options | Lifetime coverage | Death benefit, cash value accumulation (growth depends on investment performance), potential for higher returns but also higher risk | Individuals comfortable with investment risk and seeking potential for higher returns |

Understanding Your Needs

Choosing the right life insurance policy isn’t about picking the cheapest option; it’s about securing your family’s financial future. A well-chosen policy provides a safety net, protecting loved ones from the financial burden that can follow an unexpected loss. Understanding your individual financial situation and future goals is paramount in making an informed decision.

Assessing your current financial standing and projecting your future needs is crucial for determining the appropriate coverage amount. This involves carefully considering your existing debts, future financial goals, and the needs of your dependents. Failing to accurately assess these factors can lead to inadequate coverage, leaving your family vulnerable. Conversely, over-insuring can result in unnecessary expenses.

Determining the Appropriate Death Benefit

The death benefit, the amount your beneficiaries receive upon your death, should be sufficient to cover your outstanding financial obligations and provide for your dependents’ future needs. This requires a comprehensive evaluation of your financial situation. Consider factors such as outstanding mortgages, outstanding loans, credit card debts, and any other financial obligations. Additionally, factor in the cost of raising children, including education expenses, and providing for your spouse or partner’s financial security, potentially including their retirement needs. For example, a family with a $300,000 mortgage, $50,000 in other debts, and two children requiring $200,000 for college education would need a significantly larger death benefit than a single individual with no dependents and minimal debt.

Calculating Life Insurance Needs: A Step-by-Step Guide

A systematic approach is essential when calculating your life insurance needs. This process involves several key steps to ensure you secure adequate coverage.

- Calculate Total Debt: List all outstanding debts, including mortgages, loans, and credit card balances. Add these amounts to arrive at your total debt.

- Estimate Future Expenses: Consider future expenses such as children’s education, your spouse’s retirement, and any other anticipated major expenditures. Use realistic figures based on current costs and projected inflation.

- Factor in Replacement Income: Determine the amount of income your family would need to maintain their current lifestyle in your absence. Consider your current income, potential salary increases, and anticipated living expenses.

- Calculate Total Needs: Add your total debt, future expenses, and replacement income to determine your total insurance needs. This figure represents the minimum death benefit you should consider.

- Adjust for Inflation: Consider the impact of inflation on future expenses. It’s prudent to adjust your calculations to account for the rising cost of living over time. For example, using an average inflation rate of 3%, a $100,000 expense today may cost $134,392 in ten years. This calculation can be done using a compound interest formula:

Future Value = Present Value * (1 + inflation rate)^number of years

- Review and Adjust Regularly: Life circumstances change. Regularly review and adjust your life insurance needs as your family’s financial situation evolves, such as the birth of a child, changes in income, or significant debt reduction.

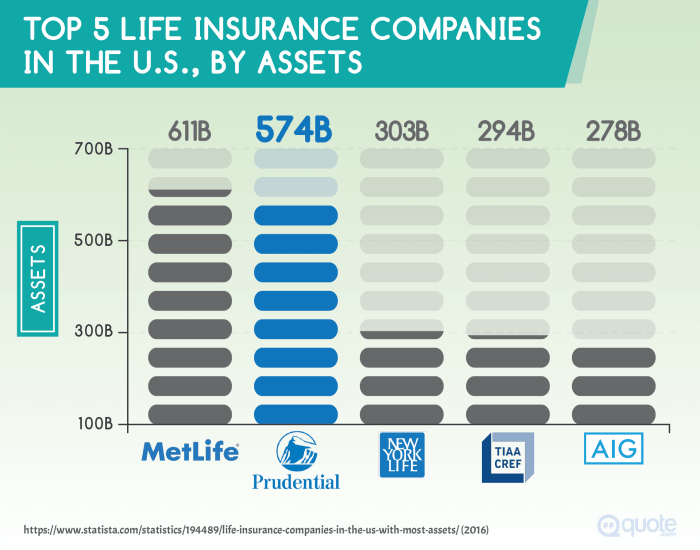

Comparing Policy Providers

Choosing the right life insurance provider is crucial, as it directly impacts the coverage you receive and the premiums you pay. A thorough comparison of different companies, considering their offerings, financial stability, and customer service, is essential for making an informed decision. This section will guide you through comparing several major providers to help you find the best fit for your needs.

Several factors influence the selection of a life insurance provider beyond the price. Understanding these factors and comparing them across different companies is vital to ensure you’re making a financially sound and reliable choice.

Provider Feature and Pricing Comparison

The following table compares three major life insurance providers – these are examples and should not be considered an exhaustive list or endorsement. Always conduct your own thorough research before making a decision. Premium costs and policy details are subject to change based on individual circumstances and the insurer’s current offerings.

| Company Name | Policy Options | Premiums (Example: 30-year-old male, $500,000 coverage) | Customer Reviews (Based on independent review sites, averaged) | Financial Strength Rating (e.g., AM Best) |

|---|---|---|---|---|

| Example Company A | Term Life, Whole Life, Universal Life | $50 – $100 per month (Illustrative range) | 4.5 stars (Illustrative) | A+ (Illustrative) |

| Example Company B | Term Life, Whole Life | $40 – $90 per month (Illustrative range) | 4.2 stars (Illustrative) | A (Illustrative) |

| Example Company C | Term Life, Universal Life, Variable Life | $60 – $120 per month (Illustrative range) | 4 stars (Illustrative) | A- (Illustrative) |

Note: The premium ranges provided are illustrative examples only and will vary greatly depending on factors such as age, health, smoking status, coverage amount, and policy type. Customer review scores are representative averages from various online review platforms and may fluctuate. Financial strength ratings are based on independent rating agencies and are subject to change.

Importance of Financial Stability and Customer Service

Selecting a financially stable provider is paramount. A company with a strong financial rating, such as those provided by AM Best, demonstrates its ability to meet its long-term obligations. This ensures that your beneficiaries will receive the death benefit when the time comes. Furthermore, a company with high customer service ratings suggests a positive experience throughout the policy lifecycle, from application to claims processing. Negative experiences can be significantly stressful during difficult times.

Policy Features and Riders

Choosing the right life insurance policy involves understanding not only the basic coverage but also the various features and riders that can enhance its value and tailor it to your specific needs. These additions often come with extra costs, but the potential benefits can significantly outweigh the expense, providing crucial financial protection for unforeseen circumstances. This section will detail common policy features and riders, explaining their functions and implications.

Accidental Death Benefit Rider

An accidental death benefit rider provides an additional payout to your beneficiaries if your death results from an accident. This supplementary payment is typically a multiple of the policy’s death benefit, for example, double or triple the original amount. The cost of this rider varies depending on factors such as your age, health, and the amount of additional coverage. The benefit lies in providing a larger financial safety net for your loved ones in the event of a sudden and unexpected death. For instance, if your policy has a $500,000 death benefit and you have a double indemnity rider, your beneficiaries would receive $1,000,000 upon your accidental death.

Critical Illness Rider

The critical illness rider offers a lump-sum payment if you are diagnosed with a specified critical illness, such as cancer, heart attack, or stroke. This payment can help cover medical expenses, lost income, and other related costs associated with a serious illness. The cost of this rider depends on factors like your age, health, and the specific illnesses covered. The benefit is the financial assistance provided during a difficult and expensive time, allowing you to focus on your health and recovery rather than worrying about immediate financial burdens. A hypothetical example: A $100,000 critical illness rider could significantly alleviate the financial strain of a lengthy cancer treatment.

Long-Term Care Rider

A long-term care rider provides benefits to cover the costs of long-term care services, such as nursing home care or in-home assistance, if you become chronically ill or disabled. This can help protect your assets and ensure you receive the necessary care without depleting your savings. The cost of this rider is determined by factors including your age, health, and the level of coverage selected. The benefit is the financial security it offers against the potentially substantial costs of long-term care, which can easily exceed hundreds of thousands of dollars over time. Consider a scenario where someone requires assisted living for several years; the long-term care rider could cover a significant portion of these expenses.

Cash Value Accumulation

Certain life insurance policies, particularly whole life and universal life policies, build cash value over time. This cash value grows tax-deferred and can be accessed through loans or withdrawals. The rate of growth varies depending on the policy and the insurer’s investment performance. The implication is that the policy serves as both a death benefit and a savings vehicle. This accumulated cash value can be used for various purposes, such as funding education, retirement, or unexpected expenses, without surrendering the death benefit.

Loan Options

Policyholders can often borrow against the accumulated cash value of their life insurance policy. These loans typically accrue interest, but they don’t require repayment as long as the policy remains in force. The implication is that you can access funds without surrendering the policy or its death benefit. However, it’s crucial to understand the interest rates and potential implications on the policy’s overall value.

Dividend Payouts

Some participating whole life insurance policies pay dividends to policyholders. These dividends are not guaranteed and are dependent on the insurer’s profitability. They can be taken as cash, used to reduce premiums, added to the cash value, or left to accumulate with interest. The benefit is a potential return on investment, further enhancing the value of the policy. However, relying on dividend payouts as a guaranteed feature is unwise, as they are not guaranteed.

Incorporating Riders and Features into a Hypothetical Policy

Let’s consider a hypothetical scenario: A 40-year-old professional, Sarah, wants life insurance to protect her family. She desires a $500,000 death benefit and is considering adding riders to address specific concerns. Given her age and health, she might choose a whole life policy for its cash value accumulation. She might add an accidental death benefit rider (doubling the benefit to $1,000,000), a critical illness rider ($100,000), and a long-term care rider ($100,000 annually for a specified period). This combination provides comprehensive coverage for various life events, offering financial security for her family in case of death, critical illness, or the need for long-term care. The cost of these additions will increase her premiums, but the enhanced protection aligns with her specific needs and risk profile. The exact costs would depend on the insurance provider and specific terms of each rider.

The Application Process

Applying for life insurance might seem daunting, but understanding the process can make it significantly less stressful. It typically involves several key steps, from completing an application to undergoing a medical evaluation, ultimately leading to policy approval and premium determination. The entire process is designed to assess your risk profile and determine the appropriate level of coverage and cost.

The application process begins with completing a detailed application form. This form requests extensive personal and health information, including your age, occupation, lifestyle habits (such as smoking), family medical history, and details about any existing health conditions. Accurate and thorough completion of this form is crucial for a smooth and efficient application process. Providing false or misleading information can lead to delays or even policy rejection.

Medical Examinations and Underwriting

Following the submission of your application, the insurer may require a medical examination. This typically involves a physical exam conducted by a physician or nurse chosen by the insurance company. The exam may include blood and urine tests, electrocardiograms (ECGs), and other assessments depending on your age, health history, and the amount of coverage you’re seeking. The purpose of this examination is to verify the information you provided on the application and to assess your overall health status. This information is then used by underwriters to evaluate your risk profile. Underwriting involves a comprehensive review of your application, medical records (if applicable), and other relevant information to determine your insurability and the appropriate premium rate.

Factors Influencing Approval and Premium Rates

Several factors influence the approval process and the final premium rates. Your age is a primary factor, as older individuals generally have a higher risk of mortality. Your health history, including pre-existing conditions and family medical history, plays a significant role. Lifestyle choices such as smoking, excessive alcohol consumption, and lack of physical activity can also increase your premiums. Your occupation, particularly if it involves hazardous work, can influence the risk assessment. Finally, the amount of coverage you seek impacts your premium; larger coverage amounts naturally result in higher premiums. For example, a 30-year-old non-smoker in good health applying for a $250,000 policy will likely receive a lower premium than a 55-year-old smoker with a history of heart disease applying for the same coverage.

Reasons for Policy Rejection and Mitigation Strategies

While most applicants are approved, policies can be rejected for various reasons. These include providing inaccurate information on the application, having a serious pre-existing medical condition that poses a high risk to the insurer, engaging in high-risk activities, or failing to meet the insurer’s underwriting requirements. To mitigate these risks, it’s essential to be completely honest and accurate on your application. If you have pre-existing health conditions, it’s advisable to disclose them upfront and discuss your options with an insurance agent. Consider improving your lifestyle choices, such as quitting smoking or adopting a healthier diet, to improve your insurability. Additionally, working with an experienced insurance agent can help you navigate the process and choose a policy that best suits your circumstances and risk profile. They can guide you through the application process and help you address any potential concerns proactively.

Long-Term Considerations

Life insurance, while often purchased with a specific short-term goal in mind, is a long-term commitment that requires periodic review and adjustment to ensure it continues to meet your evolving needs. Failing to do so could leave you with inadequate coverage when you need it most, or paying for more coverage than is necessary. Regular review ensures your policy remains a valuable asset throughout your life.

Your life insurance policy shouldn’t be a static document. As your circumstances change, so too should your coverage. Regularly assessing your policy allows you to adapt to life’s milestones and maintain appropriate protection for your loved ones. This proactive approach helps safeguard your financial future and minimizes potential gaps in coverage that could arise from unforeseen events.

Situations Requiring Policy Adjustments

Significant life events often necessitate a review of your life insurance policy. These changes can dramatically alter your financial responsibilities and the level of protection required for your dependents. Examples include marriage, which may introduce a new spouse’s financial needs into the equation; divorce, which may alter beneficiary designations and coverage amounts; the birth of a child, which significantly increases financial obligations; and career changes, which can impact your income and, consequently, your insurance needs. For instance, a promotion might justify increasing your coverage to reflect your higher earning potential, while a career shift to self-employment might require a more comprehensive policy. Similarly, purchasing a home or taking on substantial debt also warrants a policy review.

Policy Review Checklist

Regularly reviewing your life insurance policy is crucial for maintaining adequate coverage. A structured approach ensures no important aspects are overlooked. This checklist provides a framework for your review:

- Current Coverage Amount: Is the death benefit still sufficient to cover your family’s financial needs, considering inflation and potential future expenses like college tuition or retirement? Consider your outstanding debts, mortgage, and future financial goals.

- Beneficiary Designations: Are your beneficiaries still appropriate? Have there been any significant changes in your family structure, such as marriage, divorce, or the birth of a child? Ensure your beneficiaries reflect your current wishes.

- Policy Type: Is your current policy type (term, whole, universal, etc.) still aligned with your financial goals and risk tolerance? A term life policy might be suitable for short-term needs, while a whole life policy offers long-term coverage and cash value accumulation.

- Premium Payments: Can you comfortably afford your current premium payments? Consider your current income and budget to ensure the policy remains manageable. Explore options like increasing the premium to increase coverage or adjusting the policy to lower the premium.

- Health Status: Has your health status changed since you purchased the policy? Significant health changes may impact your ability to obtain or maintain coverage at the same premium.

- Financial Goals: Have your financial goals changed? Factors like buying a house, starting a family, or retirement planning significantly impact insurance needs.

Illustrative Examples

Choosing the right life insurance policy is a deeply personal decision, heavily influenced by individual circumstances and financial goals. The following scenarios illustrate how different life stages and priorities lead to different policy selections.

Term Life Insurance for a Young Family

A young couple, Sarah (30) and John (32), have two young children and a mortgage. Sarah is a teacher, and John works in construction. Their primary financial concern is ensuring their children’s financial security and paying off their mortgage should either parent pass away. They choose a 20-year term life insurance policy with a death benefit of $500,000. This amount is sufficient to cover their mortgage, provide for their children’s education, and maintain their family’s living expenses for a significant period. They opt for a term policy because it offers affordable coverage for a specified period, aligning with their need for protection while their mortgage and childcare expenses are high. The policy’s relatively low premiums allow them to allocate more of their budget to other financial goals. No riders are added at this time, as their primary need is straightforward financial protection.

Whole Life Insurance for an Individual Nearing Retirement

Robert (60), a successful businessman, is nearing retirement. He has substantial assets but wants to ensure a legacy for his family and to provide for his spouse, Mary (58), after his passing. He chooses a whole life insurance policy with a death benefit of $1 million. This policy provides lifelong coverage and builds cash value over time. The cash value component allows Robert to access funds for potential future needs, offering a degree of financial flexibility during retirement. He adds a long-term care rider to help cover potential costs associated with nursing home care in his later years. This demonstrates a focus not only on leaving a substantial inheritance but also on mitigating potential financial burdens associated with aging. The higher premiums reflect the lifelong coverage and the added rider, but they align with Robert’s long-term financial security and legacy planning objectives.

Conclusive Thoughts

Ultimately, selecting the best life insurance policy is a deeply personal journey. It requires careful consideration of your current financial standing, future aspirations, and the needs of your dependents. By understanding the nuances of different policy types, comparing providers, and regularly reviewing your coverage, you can confidently navigate this important decision and create a secure financial legacy for those you cherish. Remember, proactive planning today translates to peace of mind tomorrow.

Query Resolution

What is the difference between term and whole life insurance?

Term life insurance provides coverage for a specific period (term), offering lower premiums but no cash value accumulation. Whole life insurance offers lifelong coverage with a cash value component that grows over time, but with higher premiums.

How much life insurance do I really need?

Your life insurance needs depend on factors like outstanding debts (mortgage, loans), dependents’ future expenses (education, living costs), and your desired legacy. Financial advisors can help you determine the appropriate coverage amount.

Can I change my life insurance policy later?

Depending on the policy type and the insurer, you may be able to adjust your coverage amount, add riders, or change beneficiaries. Contact your insurer to understand your options.

What happens if my application is rejected?

Rejection often stems from health issues or insufficient information. You can reapply after addressing the concerns raised by the insurer, or explore alternative insurance options.