Finding the best car insurance in Texas can feel overwhelming, given the sheer number of providers and varying coverage options. This guide navigates the complexities of the Texas car insurance market, helping you make an informed decision based on factors like cost, customer service, and coverage types. We’ll explore the top companies, key influencing factors on premiums, and essential details to consider before committing to a policy.

Understanding your needs and comparing options is crucial. We’ll delve into the nuances of different coverage types, highlighting the minimum requirements mandated by Texas law and the benefits of optional add-ons. By examining customer reviews and understanding policy details, you can confidently choose a provider that aligns with your budget and risk tolerance. We also explore ways to potentially lower your premiums and maximize savings.

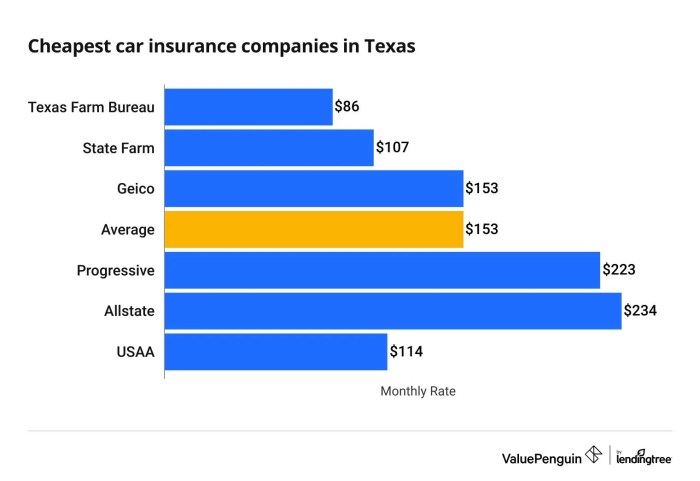

Top Texas Car Insurance Providers

Choosing the right car insurance in Texas can feel overwhelming, given the numerous providers vying for your business. This section will highlight some of the most prominent companies and offer a comparison to aid in your decision-making process. Remember that rates and services can vary significantly based on individual factors like driving history, location, and the type of vehicle insured.

Understanding the landscape of Texas car insurance requires examining the market leaders. While precise market share figures fluctuate, consistent data reveals a clear group of dominant players. The following list represents ten frequently mentioned car insurance companies operating extensively in Texas, though their exact ranking may vary depending on the source and year.

Ten Frequently Mentioned Texas Car Insurance Companies

This list is not exhaustive and the order does not reflect a specific ranking. The relative prominence of these companies is based on their widespread presence and frequent mention in consumer reports and industry analyses.

- State Farm

- GEICO

- USAA

- Progressive

- Allstate

- Farmers Insurance

- Nationwide

- Liberty Mutual

- AAA

- Auto-Owners Insurance

Market Share and History of Top Three Texas Car Insurance Companies

Focusing on the top three providers offers a deeper insight into their market dominance and operational history. This analysis is based on publicly available information and industry reports, and precise figures may vary.

State Farm: A long-standing giant in the insurance industry, State Farm boasts a significant market share in Texas, built over decades of consistent service and a vast agent network. Its history dates back to the 1920s, establishing a strong foundation of trust and brand recognition. Their extensive reach and broad range of insurance products contribute to their continued success.

GEICO: Known for its aggressive marketing and competitive pricing, GEICO has rapidly expanded its presence in Texas and across the nation. GEICO’s history is marked by innovative approaches to customer service and technology, often leveraging online platforms and direct-to-consumer strategies. Their focus on efficiency and cost-effectiveness has made them a formidable competitor.

USAA: While not as broadly accessible as State Farm or GEICO, USAA holds a substantial market share among eligible members (primarily military personnel and their families). USAA’s history is deeply rooted in serving the military community, building a reputation for excellent customer service and competitive rates. Their exclusive membership model contributes to their high customer satisfaction scores.

Comparison of Top Three Texas Car Insurance Companies

The following table offers a simplified comparison of State Farm, GEICO, and USAA across key metrics. These figures are averages and individual experiences may differ significantly. It is crucial to obtain personalized quotes from each company for accurate cost estimations.

| Company | Average Annual Premium (Estimate) | Customer Satisfaction Rating (J.D. Power, Example) | Claims Processing Speed (Average, Example) |

|---|---|---|---|

| State Farm | $1200 | 850 | 10-14 days |

| GEICO | $1100 | 820 | 7-10 days |

| USAA | $1300 | 900 | 5-7 days |

Note: The data presented in the table is for illustrative purposes only and should not be considered definitive. Actual premiums, ratings, and processing speeds will vary based on individual circumstances and may change over time. Always refer to the latest information from independent sources and the insurance companies themselves.

Factors Influencing Car Insurance Costs in Texas

Securing affordable car insurance in Texas depends on a variety of factors. Understanding these factors can help drivers make informed decisions and potentially lower their premiums. Insurance companies use a complex algorithm to assess risk, and the resulting premium reflects that assessment.

Several key elements contribute significantly to the final cost of your car insurance. These include your driving history, age, location, the type of vehicle you drive, and even your credit score in some cases. The interaction of these factors creates a unique profile for each driver, leading to a personalized premium.

Driving Record

Your driving history is arguably the most significant factor determining your car insurance rates. A clean driving record with no accidents or violations will result in lower premiums compared to a record marred by multiple incidents. The severity of violations also plays a crucial role. For example, a speeding ticket will generally have a less severe impact than a DUI or a collision resulting in significant property damage or injury. Different insurance companies may weigh these violations differently, leading to variations in premium increases. A single at-fault accident can lead to a substantial increase, potentially doubling or tripling your premiums depending on the circumstances and the insurer. Multiple accidents or serious violations can lead to even higher increases or even policy cancellation in some cases.

Age and Driving Experience

Younger drivers, particularly those under 25, generally pay higher premiums due to statistically higher accident rates within this demographic. Insurance companies perceive this group as higher risk. As drivers gain experience and age, their premiums typically decrease, reflecting a reduced risk profile. This is because experience often correlates with better driving habits and fewer accidents. Mature drivers, generally over 50, often benefit from lower rates, assuming a clean driving record.

Location

Your geographic location significantly influences your insurance rates. Areas with high crime rates, a higher frequency of accidents, or more vehicle thefts will typically have higher insurance premiums due to the increased risk to insurance companies. Urban areas often have higher rates than rural areas due to factors like increased traffic congestion and higher likelihood of theft.

Vehicle Type

The type of vehicle you drive is another critical factor. Sports cars, luxury vehicles, and high-performance cars are generally more expensive to insure due to their higher repair costs and greater potential for damage. The vehicle’s safety features also play a role. Cars with advanced safety technology, such as anti-lock brakes and airbags, may qualify for discounts. Similarly, the vehicle’s age and condition can affect premiums; older cars may be cheaper to insure but might not offer the same safety features.

Ways to Lower Car Insurance Premiums

Many strategies can help drivers reduce their car insurance costs.

- Maintain a clean driving record: Avoid speeding tickets, accidents, and other violations.

- Shop around and compare quotes from multiple insurers: Different companies use different rating systems.

- Consider increasing your deductible: A higher deductible means lower premiums, but you’ll pay more out-of-pocket in the event of a claim.

- Bundle your insurance policies: Combining auto insurance with home or renters insurance can often result in discounts.

- Take a defensive driving course: Successfully completing a course can demonstrate your commitment to safe driving and earn you a discount.

- Install anti-theft devices: These can reduce the risk of theft and potentially lower your premiums.

- Maintain good credit: In some states, including Texas, your credit score can be a factor in determining your insurance rates.

Types of Car Insurance Coverage in Texas

Choosing the right car insurance coverage in Texas is crucial for protecting yourself financially in the event of an accident. Understanding the different types of coverage available and the state’s minimum requirements will help you make an informed decision that suits your needs and budget. This section details the various coverage options and their implications.

Liability Coverage

Liability insurance covers damages you cause to others in an accident. This is the most basic type of car insurance and is required by Texas law. It protects you against financial responsibility for injuries or property damage you inflict on others. Liability coverage typically includes bodily injury liability, which covers medical expenses and lost wages for injured parties, and property damage liability, which covers repairs or replacement costs for damaged vehicles or property. The minimum liability coverage required in Texas is 30/60/25, meaning $30,000 per person for bodily injury, $60,000 per accident for bodily injury, and $25,000 for property damage. However, carrying higher liability limits is strongly recommended, as a serious accident could easily exceed these minimums. For example, a severe accident involving multiple injuries could easily lead to claims exceeding $60,000. Failing to carry adequate liability coverage could leave you personally liable for significant financial losses.

Collision Coverage

Collision coverage pays for repairs or replacement of your vehicle regardless of fault. This means that even if you cause the accident, your insurance will cover the damage to your car. It’s optional coverage, but it offers significant protection against the potentially high costs of vehicle repairs or replacement. The deductible you choose will influence the amount you pay out-of-pocket. A higher deductible typically leads to lower premiums. For instance, a $500 deductible means you pay the first $500 of repair costs, while your insurer covers the rest.

Comprehensive Coverage

Comprehensive coverage protects your vehicle against damage caused by events other than collisions, such as theft, vandalism, fire, hail, or natural disasters. Like collision coverage, it’s optional, but it provides broad protection against a wide range of potential risks. Again, a deductible applies, affecting the out-of-pocket expenses. Consider the value of your vehicle when deciding whether this coverage is worthwhile. A newer, more expensive car might benefit more from comprehensive coverage than an older, less valuable one.

Uninsured/Underinsured Motorist Coverage

This coverage protects you if you’re involved in an accident caused by an uninsured or underinsured driver. It covers your medical expenses, lost wages, and vehicle repairs. Texas law requires insurers to offer this coverage, but you can choose to reject it in writing. However, it’s highly recommended to carry this protection, as accidents involving uninsured drivers are unfortunately common. Consider the potential financial burden of medical bills and vehicle repairs if you are injured by an uninsured driver without this coverage.

Customer Reviews and Ratings

Understanding customer reviews is crucial when choosing a car insurance provider. Online platforms like Yelp and Google Reviews offer a wealth of information reflecting real customer experiences, allowing for a more informed decision beyond advertised rates and coverage options. Analyzing this feedback can reveal strengths and weaknesses in areas like claims processing and customer service, providing valuable insights into a company’s overall reliability and responsiveness.

Analyzing customer reviews from various online platforms provides a comprehensive picture of each insurer’s performance. By categorizing feedback based on specific aspects of the customer journey, we can identify recurring themes and trends, ultimately helping consumers make more informed choices.

Claims Handling Experiences

Claims handling is a critical aspect of car insurance, and customer reviews often highlight the efficiency and fairness of this process. A review analysis might reveal that Company A consistently receives positive feedback for their quick response times and straightforward claims settlements, while Company B might show a higher incidence of complaints regarding lengthy processing times and difficulties in reaching customer service representatives. These discrepancies are significant and directly impact the customer experience during a stressful time. For example, a common theme might be the speed of claim approval and payment. Another recurring theme could be the clarity of communication throughout the claims process.

Customer Service Interactions

Customer service quality significantly impacts the overall customer experience. Reviews frequently discuss the responsiveness, helpfulness, and professionalism of customer service representatives. Positive reviews often praise easy-to-navigate websites, readily available phone support, and knowledgeable agents. Conversely, negative reviews might describe difficulties in contacting representatives, unhelpful or dismissive responses, and long wait times. For instance, one common trend might be the accessibility of customer service channels, with some companies receiving praise for their 24/7 availability and others criticized for limited hours or unresponsive email support. Another trend might be the level of agent expertise in resolving customer queries.

Comparative Analysis of Top Three Companies

Let’s consider three hypothetical top Texas car insurance companies – “Statewide Secure,” “Texas Shield,” and “Lone Star Auto.” Analysis of their online reviews might reveal that Statewide Secure consistently receives high marks for efficient claims processing but lower ratings for customer service responsiveness. Texas Shield might receive average scores across both categories, suggesting a balanced performance. Lone Star Auto, conversely, could show excellent customer service reviews but some negative feedback regarding claims processing speed. This comparative analysis allows consumers to weigh the relative importance of these factors based on their individual priorities. For example, a customer prioritizing fast claims processing might favor Statewide Secure despite the less positive customer service reviews, while a customer who values excellent customer service might choose Lone Star Auto despite the potential for slower claims handling. This highlights the importance of individualized assessment based on personal needs and preferences.

Understanding Policy Details and Fine Print

Before committing to a car insurance policy in Texas, meticulously reviewing the policy documents is crucial. Failing to understand the details can lead to unexpected costs and inadequate coverage when you need it most. This section highlights key aspects to consider and strategies for navigating the often complex policy language.

Insurance policies, while necessary, are notoriously dense and filled with legal jargon. Taking the time to understand the fine print can save you significant financial stress down the line. Don’t hesitate to ask your insurance agent for clarification on anything you don’t understand; it’s their job to help you comprehend your policy.

Common Policy Exclusions and Limitations

Many policies exclude specific events or circumstances from coverage. Understanding these exclusions is vital to avoid surprises. For instance, damage caused by wear and tear is typically not covered, nor are damages resulting from driving under the influence of alcohol or drugs. Similarly, many policies have limitations on coverage amounts for specific types of damages or losses. For example, there might be a lower payout for claims related to rental car damage compared to damage to your personal vehicle. Some policies also might limit coverage for accidents outside a specified geographic area.

Understanding Deductibles and Premiums

Your deductible is the amount you pay out-of-pocket before your insurance coverage kicks in. A higher deductible generally leads to lower premiums (the amount you pay regularly for insurance), while a lower deductible means higher premiums. Understanding this relationship is key to finding a balance that suits your budget and risk tolerance. For example, a $500 deductible might result in a lower monthly premium than a $1000 deductible, but you’ll pay more out-of-pocket if you file a claim. Conversely, a higher deductible will lower your monthly payment but increase your financial responsibility in case of an accident.

Tips for Understanding and Negotiating Policy Terms

Begin by reading the policy summary carefully, focusing on key terms like coverage limits, deductibles, and exclusions. Then, carefully review the full policy document, section by section, taking notes and highlighting any unclear or concerning clauses. If you find terms you don’t understand, contact your insurance agent or company directly for clarification. While negotiating specific policy terms might be challenging, you can often negotiate your premium by comparing quotes from different insurers, bundling policies (home and auto), or demonstrating a good driving record. Maintaining a clean driving history is a significant factor in securing lower premiums. Consider exploring discounts offered for safety features in your vehicle, such as anti-theft devices or advanced driver-assistance systems.

Filing a Claim with Texas Car Insurance Companies

Filing a car insurance claim in Texas can seem daunting, but understanding the process can make it significantly smoother. This section Artikels the typical steps involved, necessary documentation, and provides a general comparison of claims processes across different insurers. Remember that specific procedures may vary slightly depending on your insurance provider and the specifics of your accident.

The process generally begins immediately after an accident. Prompt reporting is crucial for a successful claim. Timely action protects your rights and facilitates a quicker resolution.

Steps to File a Car Insurance Claim in Texas

Filing a claim typically involves these key steps. While the exact order might vary, these represent the core elements of the process.

- Report the Accident: Contact your insurance company as soon as possible after the accident. Provide them with the essential details, including the date, time, location, and a brief description of what happened. Many companies have 24/7 claims hotlines.

- Gather Information: Collect information from all involved parties, including names, addresses, phone numbers, driver’s license numbers, insurance information, and vehicle information (make, model, year, VIN). If there are witnesses, obtain their contact information as well.

- Document the Accident: Take photos and videos of the damage to all vehicles involved, the accident scene (including road conditions and any visible signs of fault), and any visible injuries. Obtain a copy of the police report if one was filed.

- Submit Your Claim: Your insurance company will guide you through the claim submission process, which usually involves completing a claim form and providing all the collected documentation. This might be done online, by phone, or by mail.

- Cooperate with the Investigation: Your insurance company may investigate the accident to determine liability. Be prepared to answer questions and provide any additional information they request.

- Review the Settlement Offer: Once the investigation is complete, your insurance company will typically provide a settlement offer. Review it carefully and negotiate if necessary.

Required Information and Documentation

The specific documentation required may vary depending on the insurer and the circumstances of the accident, but generally includes the following. Having these ready will expedite the claims process.

- Police report (if applicable)

- Photos and videos of the accident scene and vehicle damage

- Contact information of all involved parties

- Driver’s licenses and insurance information of all involved parties

- Vehicle identification numbers (VINs)

- Medical records (if injuries are involved)

- Repair estimates (if applicable)

Comparison of Claims Processes Across Insurers

Claims processes can vary significantly between insurance companies. Some companies are known for their quicker processing times and more streamlined online portals, while others might have more traditional methods. Customer service responsiveness also differs widely. It’s advisable to research individual company reviews and ratings to get a sense of their claims handling reputation before selecting a provider. For example, some insurers may offer dedicated claims adjusters who contact you promptly, while others might have a more automated system.

For instance, a company like State Farm might be known for its extensive network of local agents and relatively quick claims processing, whereas another company might emphasize online self-service options. These differences are important to consider when choosing an insurer, especially given the importance of efficient claims handling in times of need.

Discounts and Savings Opportunities

Saving money on car insurance in Texas is achievable through various discounts offered by insurance companies. Understanding these discounts and how to qualify for them can significantly reduce your annual premiums. Many factors influence eligibility, so it’s crucial to explore all available options.

Many Texas car insurance providers offer a range of discounts designed to reward safe driving habits and responsible behavior. These can substantially lower your premiums, making insurance more affordable. By understanding these discounts and proactively meeting the requirements, you can secure significant savings.

Good Driver Discounts

Good driver discounts reward drivers with clean driving records. These discounts are typically based on the absence of accidents and traffic violations over a specific period, usually three to five years. The longer your record remains accident-free and violation-free, the greater the discount you may receive. For example, a driver with a five-year clean record might qualify for a higher percentage discount than someone with a three-year clean record. Specific requirements and discount percentages vary by insurance company.

Bundling Discounts

Bundling your car insurance with other insurance policies, such as homeowners or renters insurance, is another common way to save. Insurance companies often offer significant discounts for bundling multiple policies together. This is because it simplifies their administrative processes and reduces the risk associated with insuring multiple assets for a single customer. The discount percentage for bundling varies depending on the insurer and the specific policies bundled. For example, bundling car insurance with homeowners insurance could result in a 10-15% discount on your overall premiums.

Other Discounts

Beyond good driver and bundling discounts, numerous other opportunities exist to reduce your premiums. These may include discounts for:

- Vehicle Safety Features: Cars equipped with anti-theft devices, airbags, and other safety features often qualify for discounts due to their reduced risk profile.

- Payment Method: Paying your premium in full annually or semi-annually, rather than monthly, may result in a discount.

- Student Discounts: Good students with high GPAs may qualify for discounts, reflecting the lower risk associated with responsible young drivers.

- Military Discounts: Active military personnel and veterans often receive discounts as a token of appreciation for their service.

- Professional Affiliations: Some companies offer discounts to members of specific professional organizations or groups.

- Telematics Programs: These programs use devices or apps to monitor driving habits. Safe driving behaviors can lead to significant premium reductions.

Maximizing Car Insurance Savings

To maximize your savings, consider the following strategies:

- Shop around and compare quotes: Obtain quotes from multiple insurance companies to compare prices and coverage options.

- Maintain a clean driving record: Avoid accidents and traffic violations to qualify for good driver discounts.

- Bundle your insurance policies: Combine your car insurance with other policies to receive bundling discounts.

- Consider increasing your deductible: A higher deductible will typically result in lower premiums, but remember to have sufficient savings to cover the deductible in case of an accident.

- Explore all available discounts: Actively inquire about discounts offered by your insurer and meet the eligibility criteria.

- Review your coverage needs annually: Ensure you have the appropriate coverage for your needs without overspending.

Texas-Specific Regulations and Laws

Texas, like all states, has its own unique set of regulations and laws governing car insurance. Understanding these specifics is crucial for Texas drivers to ensure they maintain adequate coverage and comply with the law. Failure to do so can result in penalties and legal ramifications.

Texas operates under a “financial responsibility” law, meaning drivers must prove they can cover the costs of damages caused by accidents. This is typically done through carrying the minimum required car insurance coverage or by demonstrating sufficient financial resources to pay for potential damages. The state mandates specific minimum coverage amounts, and exceeding these minimums offers greater protection.

The Role of the Texas Department of Insurance (TDI)

The Texas Department of Insurance (TDI) is the state agency responsible for regulating the insurance industry within Texas. This includes overseeing car insurance companies, ensuring they maintain financial solvency, and investigating consumer complaints. The TDI sets and enforces regulations, approves insurance rates, and works to protect consumers’ rights. They provide resources and information to help Texans understand their insurance options and navigate any disputes with their insurers. The TDI also licenses and monitors insurance agents and companies operating within the state, maintaining a degree of oversight to ensure fair practices.

Resolving Insurance Disputes in Texas

If a dispute arises between a policyholder and their car insurance company in Texas, several avenues exist for resolving the issue. Initially, attempting to resolve the issue directly with the insurance company is recommended. Many companies have internal dispute resolution processes. If this fails, consumers can file a complaint with the TDI. The TDI investigates complaints, mediating between the parties whenever possible. If mediation is unsuccessful, consumers may pursue other legal options, such as arbitration or filing a lawsuit in civil court. The choice of approach depends on the nature and severity of the dispute and the amount of money involved. The TDI website provides detailed information on filing complaints and the various dispute resolution options available to Texas residents.

End of Discussion

Securing affordable and comprehensive car insurance in Texas requires careful consideration of various factors. By understanding the key elements discussed – from choosing among top providers and evaluating coverage options to navigating claims processes and maximizing savings – you’re empowered to make a well-informed choice. Remember to compare quotes, read policy documents thoroughly, and don’t hesitate to seek clarification on any aspects you find unclear. Your safety and financial security are paramount.

Popular Questions

What is SR-22 insurance in Texas?

SR-22 insurance is proof of financial responsibility required by the state of Texas for drivers with certain driving violations, like DUI convictions. It certifies you have the minimum liability coverage required by law.

Can I get car insurance without a driver’s license?

Generally, no. Most Texas insurers require a valid driver’s license to obtain car insurance. However, some exceptions may exist depending on the specific circumstances and the insurer’s policies.

How often can I change my car insurance company?

You can typically switch car insurance companies whenever your current policy expires. Many companies allow cancellation with a short notice period, but early cancellation fees may apply.

What happens if I get into an accident and don’t have insurance?

Driving without insurance in Texas is illegal and carries significant penalties, including fines, license suspension, and potential legal action from the other party involved in the accident.