Securing affordable auto insurance in Florida can feel like navigating a complex maze. This guide unravels the intricacies of the Sunshine State’s insurance market, providing insights into factors influencing costs, strategies for securing lower premiums, and essential details to understand your policy. We’ll explore various coverage options, compare average premiums across major cities, and arm you with the knowledge to make informed decisions.

From understanding the impact of your driving history to leveraging discounts and negotiating with insurers, we’ll equip you with the tools to find the best and most affordable auto insurance that fits your needs. We’ll also address common misconceptions and offer practical advice to help you save money without compromising crucial coverage.

Understanding Florida’s Auto Insurance Market

Navigating the Florida auto insurance market can be complex, with a variety of factors influencing the cost of coverage and a range of policy options available. Understanding these factors and the different types of coverage is crucial for securing affordable and adequate protection. This section will clarify the key aspects of the Florida auto insurance landscape.

Factors Influencing Auto Insurance Costs in Florida

Several key factors contribute to the overall cost of auto insurance in Florida. These include the driver’s driving record (accidents and traffic violations significantly impact premiums), age and gender (younger drivers and males generally pay more), vehicle type and value (sports cars and luxury vehicles are more expensive to insure), location (insurance rates vary considerably across different cities and counties due to varying accident rates and crime statistics), and credit history (in many states, including Florida, insurers use credit-based insurance scores to assess risk). Furthermore, the type of coverage selected and the amount of coverage chosen also significantly influence the final premium. For example, higher liability limits will result in higher premiums, but offer greater financial protection in the event of an accident.

Types of Auto Insurance Coverage Available in Florida

Florida law mandates specific minimum coverage levels, but drivers can opt for additional coverage for more comprehensive protection. The primary types of coverage include Bodily Injury Liability (covering injuries to others in an accident), Property Damage Liability (covering damage to others’ property), Personal Injury Protection (PIP, covering medical bills and lost wages for the insured and passengers regardless of fault), and Uninsured/Underinsured Motorist (UM/UIM) coverage (protecting the insured in accidents involving drivers without adequate insurance). Comprehensive coverage protects against damage to your vehicle from non-collision events (like theft or hail), while Collision coverage protects against damage from accidents.

Minimum Coverage Requirements Versus Recommended Coverage

Florida’s minimum coverage requirements are $10,000 for Property Damage Liability and $10,000 for Bodily Injury Liability per person, with a total of $20,000 for Bodily Injury Liability per accident. However, these minimums are often insufficient to cover significant medical expenses or property damage in a serious accident. Many financial advisors recommend higher liability limits, such as $100,000/$300,000 (meaning $100,000 per person and $300,000 per accident for Bodily Injury Liability) and at least $50,000 for Property Damage Liability. Adding Uninsured/Underinsured Motorist coverage is also highly recommended, given the high number of uninsured drivers in Florida. Comprehensive and Collision coverage, while not mandatory, provide essential protection against damage to your own vehicle.

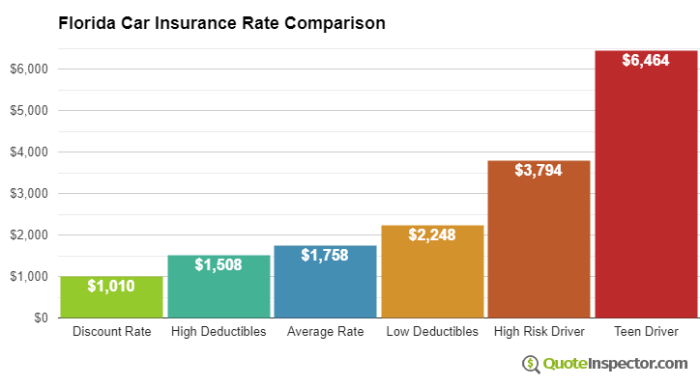

Average Premiums Across Major Florida Cities

The following table provides a comparison of average annual auto insurance premiums across several major Florida cities. These are estimates and actual premiums will vary based on individual factors.

| City | Average Annual Premium (Estimate) | Factors Influencing Cost | Notes |

|---|---|---|---|

| Miami | $2,000 – $2,500 | High accident rates, high population density, vehicle theft | Considerably higher due to high risk factors. |

| Orlando | $1,800 – $2,200 | Significant tourist traffic, large population | Rates are generally higher than smaller cities. |

| Tampa | $1,700 – $2,100 | Large metropolitan area, moderate accident rates | Similar to Orlando, reflecting the characteristics of a large city. |

| Jacksonville | $1,600 – $2,000 | Large geographic area, varied risk levels across the city | Rates can vary significantly depending on specific location within the city. |

Finding Affordable Insurance Options

Securing affordable auto insurance in Florida requires a proactive approach. Understanding your options and employing effective strategies can significantly reduce your premiums. This section will explore several key areas to help you navigate the process and find the best coverage at a price you can manage.

Finding the right balance between cost and coverage is crucial. Many factors influence your insurance rates, and understanding these allows you to make informed decisions to lower your premiums.

Strategies for Reducing Auto Insurance Premiums

Several methods can help lower your Florida auto insurance premiums. Maintaining a clean driving record is paramount. Bundling your auto insurance with other policies, such as homeowners or renters insurance, often results in discounts. Consider increasing your deductible; a higher deductible generally translates to lower premiums, though it means you’ll pay more out-of-pocket in the event of a claim. Choosing a vehicle with a good safety rating can also impact your rates favorably, as insurers often reward safer vehicles with lower premiums. Finally, exploring discounts offered for good students, safe drivers, and those who complete defensive driving courses can further reduce costs.

Driving History’s Impact on Insurance Rates

Your driving history is a significant factor determining your insurance premiums. A clean record with no accidents or traffic violations will result in lower rates. Conversely, accidents, especially those deemed your fault, and traffic violations like speeding tickets or DUIs will substantially increase your premiums. The severity of the offense directly correlates with the premium increase. For instance, a DUI conviction will typically lead to a much higher increase than a speeding ticket. Insurance companies use a points system to track driving infractions, and these points directly affect your rates. The more points accumulated, the higher the premium.

Benefits and Drawbacks of Different Insurance Companies

Florida boasts numerous auto insurance providers, each with its own strengths and weaknesses. Some companies might offer lower premiums initially but may have less favorable customer service or claims handling processes. Others might have higher premiums but offer comprehensive coverage and excellent customer support. It’s essential to compare quotes from multiple insurers, considering not just the price but also the level of coverage, customer reviews, and financial stability of the company. Larger, well-established companies often provide more financial security in the event of a significant claim, but smaller, regional companies may offer more personalized service and potentially lower rates. Independent research into company ratings and customer reviews is strongly recommended before making a decision.

Questions to Ask Potential Insurance Providers

Before committing to an insurance provider, it’s crucial to ask specific questions. Inquire about the details of their coverage, including what is and isn’t covered under their policies. Ask about their claims process, including how long it typically takes to process a claim and what documentation is required. Clarify the process for increasing or decreasing coverage, as well as any potential penalties for cancelling a policy early. It’s also important to understand the different discounts offered and the specific requirements to qualify for them. Finally, ask about their customer service availability and methods of contact, ensuring easy access to assistance when needed. Thoroughly comparing these aspects across different providers will help you find the best fit for your needs and budget.

Factors Affecting Insurance Costs

Understanding the factors that influence your auto insurance premiums in Florida is crucial for securing affordable coverage. Several key elements contribute to the final cost, and being aware of them can help you make informed decisions to potentially lower your expenses. These factors are weighed differently by each insurance company, but generally, the following are considered most important.

Several key factors determine your auto insurance rates in Florida. Insurers use a complex algorithm to assess risk and calculate premiums. These factors are not weighted equally, and some carry significantly more weight than others.

Key Factors Determining Insurance Rates

Insurers consider a range of factors when calculating your premiums. These include your age, driving history, the type of vehicle you drive, your location, and your coverage choices. Understanding how these factors interact is essential for managing your insurance costs effectively.

- Age and Driving Experience: Younger drivers, particularly those with less than three years of driving experience, are statistically more likely to be involved in accidents. This higher risk translates to higher premiums. As you gain experience and age, your premiums generally decrease.

- Driving Record: Your driving history significantly impacts your rates. Accidents, traffic violations, and even the number of points on your license contribute to higher premiums. A clean driving record is the most effective way to keep costs low.

- Vehicle Type: The type of car you drive affects your insurance cost. Sports cars and high-performance vehicles are generally more expensive to insure due to their higher repair costs and increased risk of theft. Safer, less expensive vehicles often result in lower premiums.

- Location: Where you live impacts your rates. Areas with higher crime rates or a greater frequency of accidents typically have higher insurance premiums due to increased risk.

- Coverage Choices: The level of coverage you select directly affects your premium. Comprehensive and collision coverage, while offering more protection, are more expensive than liability-only coverage.

Impact of Driving Records on Premiums

A clean driving record is paramount for securing affordable auto insurance. Even a single at-fault accident can significantly increase your premiums for several years. Multiple accidents or serious violations, such as driving under the influence (DUI), can lead to substantially higher costs or even policy cancellation. Conversely, maintaining a spotless record often leads to discounts and lower rates over time. For example, a driver with three accidents in three years might see their premiums double or triple compared to a driver with a clean record.

Prioritized List of Factors Influencing Premiums

While the precise weighting varies among insurers, a general prioritization of factors affecting premiums might look like this:

- Driving Record (Accidents, Violations)

- Age and Driving Experience

- Vehicle Type and Value

- Location (Zip Code, Risk Assessment)

- Coverage Choices (Comprehensive, Collision, Liability)

Visual Representation of Driving History and Insurance Costs

Imagine a graph with the x-axis representing the number of accidents/violations in the past three years, and the y-axis representing the insurance premium cost. The graph would show a strong positive correlation. As the number of accidents/violations increases (moving along the x-axis), the insurance premium cost (y-axis) rises sharply. A line starting low on the y-axis for a clean driving record would steeply ascend with each additional incident, illustrating the significant impact of driving history on insurance costs. For example, a point near the origin (0 accidents/violations) would represent a low premium, while a point far to the right (multiple accidents/violations) would represent a significantly higher premium.

Discounts and Savings Opportunities

Securing affordable auto insurance in Florida often hinges on understanding and leveraging the various discounts available. Many insurers offer a range of savings opportunities, allowing you to significantly reduce your premiums. By actively pursuing these discounts and comparing quotes, you can find the best possible coverage at a price that fits your budget.

Good Driver Discounts

Maintaining a clean driving record is a significant factor in obtaining lower insurance premiums. Insurers reward drivers with a history of safe driving by offering substantial discounts. These discounts are typically tiered, with larger reductions for longer periods without accidents or traffic violations. For example, a driver with five years of accident-free driving might receive a 15% discount, while ten years could result in a 25% discount, or even more depending on the insurer. To qualify, you’ll need to provide your driving history, usually through a motor vehicle report (MVR).

Bundling Discounts

Bundling your auto insurance with other types of insurance, such as homeowners or renters insurance, is a common way to save money. Many insurers offer discounts for bundling policies, as it simplifies their administration and reduces the risk associated with insuring multiple aspects of your life with a single provider. The discount percentage can vary, but it’s often in the range of 10-20%, sometimes even more. For instance, bundling your car insurance with your homeowners insurance could reduce your overall premium by 15%, resulting in significant annual savings.

Safety Feature Discounts

Modern vehicles are equipped with a variety of safety features that can reduce the risk of accidents and injuries. Insurers recognize this and often provide discounts for vehicles with features like anti-lock brakes (ABS), airbags, electronic stability control (ESC), and advanced driver-assistance systems (ADAS). The discount amount will depend on the specific features present and the insurer’s policy. A car equipped with ABS, multiple airbags, and ESC could qualify for a 5-10% discount, while vehicles with ADAS might receive even higher discounts.

Comparing Quotes from Multiple Insurers

Effectively comparing quotes is crucial for finding the most affordable insurance. Utilize online comparison tools, which allow you to input your information once and receive quotes from multiple insurers simultaneously. Carefully review each quote, paying attention not only to the premium but also to the coverage offered. Ensure you are comparing apples to apples – the same coverage limits and deductibles – before making a decision. This ensures a fair comparison and prevents choosing a cheaper policy with significantly less coverage.

Negotiating Lower Premiums

While many discounts are automatically applied, you can often negotiate lower premiums by demonstrating your commitment to safe driving and responsible insurance practices. Contact your insurer directly and inquire about potential discounts you might qualify for. Highlight any positive changes in your driving record or the addition of safety features to your vehicle. A polite and informed approach can often lead to additional savings beyond the standard discounts offered. Remember to be prepared to discuss your driving history and the specifics of your vehicle.

Understanding Policy Details

Choosing the right auto insurance policy in Florida involves understanding its key components. A comprehensive understanding of your policy’s details will help you make informed decisions and navigate any potential claims efficiently. This section Artikels the essential elements of a standard policy and the claims process.

Key Components of a Standard Auto Insurance Policy

A standard Florida auto insurance policy typically includes several crucial components. These components define the coverage you receive and the responsibilities of both the insurer and the insured. Understanding these details is vital for protecting yourself financially in the event of an accident.

- Liability Coverage: This covers bodily injury and property damage you cause to others in an accident. Florida requires minimum liability coverage of $10,000 for property damage and $10,000 per person/$20,000 per accident for bodily injury. Higher limits are recommended for greater protection.

- Personal Injury Protection (PIP): This covers your medical bills and lost wages, regardless of fault, up to the policy limits. Florida is a no-fault state, meaning PIP typically covers your injuries first, regardless of who caused the accident.

- Uninsured/Underinsured Motorist Coverage (UM/UIM): This protects you if you’re involved in an accident with an uninsured or underinsured driver. It covers your medical bills, lost wages, and property damage. It is highly recommended to carry this coverage.

- Collision Coverage: This covers damage to your vehicle caused by a collision, regardless of fault. It’s optional but highly recommended, particularly for newer vehicles.

- Comprehensive Coverage: This covers damage to your vehicle caused by events other than collisions, such as theft, vandalism, fire, or hail. This is also optional, but it provides crucial protection against various risks.

Filing a Claim in Florida

The process of filing an auto insurance claim in Florida generally involves these steps:

- Report the Accident: Immediately report the accident to the police and your insurance company. Gather information from all parties involved, including contact details, license plate numbers, and insurance information.

- Gather Evidence: Take photos of the damage to all vehicles involved, the accident scene, and any injuries. Obtain witness statements if possible.

- File a Claim: Contact your insurance company to file a formal claim, providing all the necessary information and documentation. Follow your insurer’s specific instructions for submitting your claim.

- Cooperate with the Investigation: Cooperate fully with your insurance company’s investigation of the claim. This may include providing additional information or attending an adjuster’s inspection.

- Negotiate Settlement: Once the investigation is complete, your insurance company will typically offer a settlement. You may need to negotiate to reach a fair settlement that covers all your damages.

Different Types of Coverage and Their Implications

The various coverage options within an auto insurance policy offer different levels of protection. Choosing the right coverage depends on individual needs and financial circumstances. For example, someone with a newer, expensive car might opt for higher collision and comprehensive coverage, while someone with an older car might choose lower limits. Understanding the implications of each coverage type allows for a more informed decision-making process.

Final Summary

Finding affordable auto insurance in Florida requires careful planning and research. By understanding the factors that influence premiums, actively seeking discounts, and comparing quotes from multiple insurers, you can significantly reduce your costs. Remember, securing adequate coverage is paramount, and this guide provides the foundation for making informed choices that protect both your finances and your future.

Key Questions Answered

What is the minimum required auto insurance coverage in Florida?

Florida requires minimum coverage of $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL).

Can I get car insurance if I have a bad driving record?

Yes, but it will likely be more expensive. Insurers consider your driving history, and accidents or violations can significantly impact your premiums. Consider seeking quotes from multiple insurers to find the best possible rate.

How often can I change my car insurance policy?

You can usually change your policy whenever you wish, but there may be penalties depending on your policy terms. Check your policy for details regarding cancellation fees or early termination clauses.

What is the difference between liability and collision coverage?

Liability coverage pays for damages you cause to others in an accident. Collision coverage pays for repairs to your vehicle, regardless of fault.