Securing affordable auto insurance in Illinois can feel like navigating a complex maze. Understanding the state’s minimum coverage requirements, the various types of insurance available, and the factors influencing premiums is crucial for making informed decisions. This guide unravels the intricacies of Illinois auto insurance, empowering you to find the best coverage at a price that suits your budget.

From exploring the impact of your driving record and location on your rates to uncovering potential discounts and savings, we’ll equip you with the knowledge and tools to confidently compare quotes and select the most suitable policy. We’ll also delve into resources available to help those seeking financial assistance with their insurance premiums.

Understanding Illinois Auto Insurance Requirements

Securing the right auto insurance is crucial for drivers in Illinois. Understanding the state’s minimum requirements and available coverage options helps ensure you’re adequately protected while staying within your budget. This section will clarify the different types of coverage, their associated costs, and provide a comparison to help you make informed decisions.

Illinois Minimum Liability Insurance Requirements

Illinois mandates minimum liability insurance coverage to protect others involved in accidents you cause. This coverage pays for the medical bills and property damage of the other party. The minimum requirements are $25,000 bodily injury liability per person, $50,000 bodily injury liability per accident, and $20,000 property damage liability. This means the most your insurance will pay for injuries to one person is $25,000, and the maximum payout for all injuries in a single accident is $50,000. For property damage, the maximum payout is $20,000. It’s important to understand that these minimums may not be sufficient to cover significant damages in a serious accident.

Types of Auto Insurance Coverage in Illinois

Several types of auto insurance coverage are available beyond the state-mandated minimum liability. These include:

- Liability Insurance: This covers injuries or damages you cause to others. As previously mentioned, Illinois requires minimum liability coverage, but higher limits are recommended.

- Collision Insurance: This covers damage to your vehicle in an accident, regardless of fault. This is optional but highly recommended, especially for newer vehicles.

- Comprehensive Insurance: This covers damage to your vehicle from non-accident events such as theft, vandalism, fire, or hail. This is also optional but provides broader protection.

- Uninsured/Underinsured Motorist Coverage: This protects you if you’re involved in an accident with an uninsured or underinsured driver. It covers your medical bills and property damage.

- Medical Payments Coverage (Med-Pay): This covers medical expenses for you and your passengers, regardless of fault. It can supplement health insurance.

- Personal Injury Protection (PIP): This covers medical expenses and lost wages for you and your passengers, regardless of fault. This is often required in states with “no-fault” insurance systems, but Illinois is not a no-fault state.

Cost Comparison of Auto Insurance Coverages

The cost of auto insurance varies greatly depending on factors such as your driving record, age, location, vehicle type, and the coverage levels you choose. Generally, liability insurance is the least expensive, while collision and comprehensive coverage can significantly increase your premiums. Adding optional coverages like uninsured/underinsured motorist protection will also increase the overall cost. For example, minimum liability coverage might cost around $500 annually, while adding collision and comprehensive could increase the cost to $1200 or more. These are estimates and can fluctuate based on individual circumstances.

Minimum vs. Recommended Coverage

The following table compares the minimum required coverage in Illinois with recommended coverage levels:

| Coverage Type | Minimum Required | Recommended | Cost Impact |

|---|---|---|---|

| Bodily Injury Liability per Person | $25,000 | $100,000 or more | Higher |

| Bodily Injury Liability per Accident | $50,000 | $300,000 or more | Higher |

| Property Damage Liability | $20,000 | $100,000 or more | Higher |

| Collision | Not Required | Recommended, especially for newer vehicles | Significantly Higher |

| Comprehensive | Not Required | Recommended | Higher |

| Uninsured/Underinsured Motorist | Not Required | Highly Recommended | Higher |

Factors Affecting Affordable Auto Insurance Costs in Illinois

Securing affordable auto insurance in Illinois hinges on several key factors that insurance companies meticulously assess. Understanding these factors empowers drivers to make informed choices and potentially lower their premiums. This section details the primary elements influencing your insurance costs.

Driver’s Age and Driving History

A driver’s age significantly impacts insurance premiums. Younger drivers, particularly those under 25, generally face higher rates due to statistically higher accident involvement. Insurance companies perceive them as higher risk. Conversely, older drivers with extensive safe driving records often qualify for lower rates, reflecting their lower accident probability. Driving history is equally crucial. Accidents, traffic violations, and DUI convictions all negatively affect premiums. Multiple incidents lead to significantly higher rates, reflecting the increased risk associated with a less-than-perfect driving record. For instance, a driver with a clean record for ten years might pay considerably less than a driver with two at-fault accidents and a speeding ticket within the past three years.

Geographic Location in Illinois

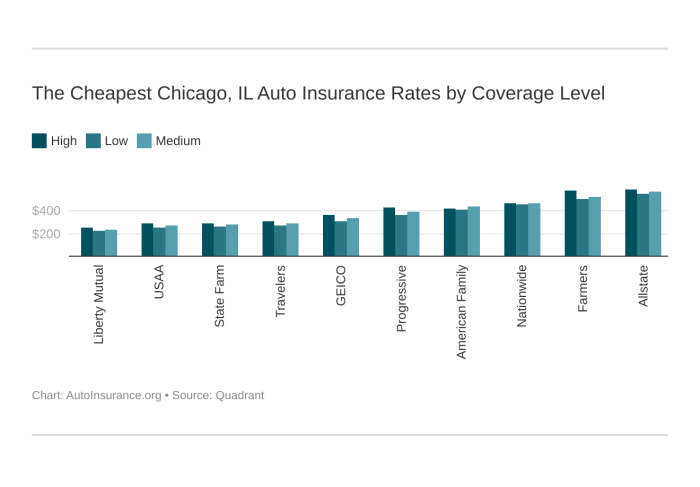

Insurance rates vary considerably across Illinois due to differences in accident frequency, crime rates, and the cost of vehicle repairs. Urban areas with higher population density and traffic congestion typically have higher insurance rates than rural areas. For example, a driver in Chicago might pay significantly more than a driver in a smaller town in southern Illinois. This is because factors like theft, vandalism, and the frequency of accidents are often higher in densely populated urban centers.

Vehicle Type

The type of vehicle you drive is a significant factor in determining insurance costs. Generally, more expensive vehicles to repair or replace command higher premiums. Sports cars and luxury vehicles often fall into this category. Conversely, less expensive vehicles like smaller sedans usually result in lower insurance costs. SUVs and trucks often sit somewhere in between, with their rates influenced by factors such as size, safety features, and theft risk. A high-performance sports car will almost always have a higher insurance premium than a fuel-efficient compact sedan.

Finding Affordable Auto Insurance Options in Illinois

Securing affordable auto insurance in Illinois requires a proactive approach to comparing quotes and understanding your options. Many resources are available to help you find the best coverage at a price that fits your budget. This section will guide you through the process of finding and comparing auto insurance quotes to ensure you obtain the most suitable and cost-effective policy.

Comparing Auto Insurance Quotes

Effectively comparing auto insurance quotes involves utilizing various methods to ensure you’re considering a wide range of providers and policies. This comparison process is crucial for finding the best value for your needs. Simply choosing the first quote you receive may not be the most financially sound decision.

Several methods exist for comparing quotes. You can contact insurance companies directly via phone or in person, request quotes through online portals, or work with an independent insurance agent who can compare options from multiple providers simultaneously. Each method offers advantages and disadvantages; the best approach depends on your personal preferences and time constraints. Directly contacting companies allows for personalized service, while online portals offer convenience and quick comparisons. Independent agents provide expertise but may not have access to every insurer.

Searching and Comparing Insurance Rates Online

The internet offers a convenient and efficient way to compare auto insurance rates from various providers. Many websites specialize in facilitating this process, allowing you to input your information once and receive multiple quotes simultaneously. This significantly reduces the time and effort required to obtain numerous quotes independently.

To effectively search online, start by using a search engine (like Google, Bing, or DuckDuckGo) and searching for “Illinois auto insurance comparison.” This will bring up a variety of websites offering quote comparison services. Enter your relevant information (address, driving history, vehicle details, etc.) accurately and completely. Be aware that some sites may require personal information before revealing full quote details. Compare the quotes you receive, paying close attention to coverage limits, deductibles, and additional fees.

Benefits and Drawbacks of Online Comparison Tools

Online insurance comparison tools offer several advantages, but also come with certain limitations. Understanding these aspects is vital for making informed decisions.

Benefits: Convenience, speed, and the ability to compare multiple quotes side-by-side are key advantages. These tools often save considerable time and effort. They can also help uncover less well-known insurers offering competitive rates.

Drawbacks: Not all insurers participate in these comparison services, meaning you might miss out on some options. The information presented might be simplified, potentially overlooking important policy details. Additionally, some websites may prioritize insurers who pay them referral fees, potentially skewing the results.

Obtaining Multiple Quotes and Choosing the Best Option

A step-by-step approach ensures you thoroughly evaluate your options and select the most appropriate auto insurance policy. Remember, the cheapest option isn’t always the best if it lacks adequate coverage.

- Gather your information: Compile all necessary information about yourself, your vehicle, and your driving history. This will streamline the quote process.

- Use online comparison tools: Utilize several online comparison websites to receive a broad range of quotes.

- Contact insurers directly: For quotes that pique your interest, contact the insurers directly to clarify any uncertainties or request additional details.

- Compare policy details: Carefully review each quote, comparing coverage limits, deductibles, premiums, and any additional fees or discounts.

- Consider your needs: Select the policy that best meets your specific needs and budget, balancing coverage adequacy with affordability. Don’t solely focus on the lowest premium; ensure you have sufficient protection.

Discounts and Savings on Illinois Auto Insurance

Securing affordable auto insurance in Illinois often involves leveraging the various discounts offered by insurance companies. Understanding these discounts and how to qualify for them is crucial for minimizing your premiums. Many factors influence the availability and amount of these discounts, so it’s beneficial to compare offers from multiple insurers.

Many Illinois auto insurance companies offer a range of discounts to help drivers lower their premiums. These discounts can significantly reduce the overall cost of insurance, making it more accessible for a wider range of individuals. Careful consideration of these options can lead to substantial savings.

Good Driver Discounts

Good driver discounts reward drivers with clean driving records. These discounts typically apply to drivers who have not been involved in accidents or received traffic violations within a specific timeframe, usually three to five years. The longer your clean driving record, the greater the potential discount. For example, a driver with a five-year accident-free history might receive a 10-20% discount, while a driver with ten years might qualify for an even higher percentage. Insurance companies use your driving history obtained from your driving record to determine eligibility.

Bundling Discounts

Bundling your auto insurance with other types of insurance, such as homeowners or renters insurance, often results in significant savings. Insurance companies incentivize bundling because it reduces their administrative costs and increases customer loyalty. The discount percentage for bundling varies depending on the insurer and the specific policies bundled, but it can easily reach 10-25% or more on your total premiums. For instance, bundling home and auto insurance with the same company could lower your overall premiums by 15%, representing a considerable saving.

Safe Driver Discounts

Some insurers offer discounts for drivers who complete defensive driving courses or participate in telematics programs. These programs track your driving habits using a device installed in your vehicle or a smartphone app. Safe driving behaviors, such as maintaining steady speeds and avoiding harsh braking or acceleration, can lead to a discount. These discounts often range from 5-15%, depending on the program and your driving performance. A driver consistently demonstrating safe driving habits through a telematics program might receive a 10% discount.

Vehicle Safety Features Discounts

Modern vehicles often come equipped with safety features such as anti-lock brakes (ABS), airbags, and electronic stability control (ESC). Insurance companies recognize that these features reduce the risk of accidents and injuries, therefore offering discounts to drivers of vehicles with such features. The discount amount varies by insurer and the specific safety features present. A vehicle with multiple advanced safety features could qualify for a 5-10% discount.

Discounts for Good Students

Many insurance companies provide discounts to students who maintain a certain grade point average (GPA). This reflects the insurer’s understanding that good students tend to be more responsible and less likely to be involved in accidents. The required GPA and the discount amount vary by insurer, but a good student discount could reduce premiums by 10-25% or more. A student maintaining a 3.5 GPA or higher could potentially receive a 15% discount.

List of Common Discounts and Eligibility Requirements

Below is a list summarizing common discounts and their associated eligibility requirements. Remember to contact your insurance provider for the most up-to-date information on specific discounts and their terms.

- Good Driver Discount: Clean driving record (typically 3-5 years without accidents or violations).

- Bundling Discount: Purchasing multiple insurance policies (e.g., auto and home) from the same insurer.

- Safe Driver Discount: Completion of a defensive driving course or participation in a telematics program.

- Vehicle Safety Features Discount: Vehicle equipped with safety features like ABS, airbags, and ESC.

- Good Student Discount: Maintaining a specific GPA (varies by insurer).

- Multi-car Discount: Insuring multiple vehicles under the same policy.

- Military Discount: Active duty military personnel or veterans.

- Senior Citizen Discount: Drivers aged 55 or older (varies by insurer).

Understanding Insurance Policies and Coverage

Understanding your auto insurance policy in Illinois is crucial for protecting yourself financially in the event of an accident. A standard policy includes several key coverages, each with its own terms and conditions, limitations, and exclusions. Familiarizing yourself with these aspects will help you make informed decisions and ensure you have the right level of protection.

Policy Terms and Conditions

Illinois auto insurance policies are legally binding contracts between you and your insurance company. These contracts Artikel the specific coverages you’ve purchased, the premiums you’ll pay, and the responsibilities of both parties. Key terms include the policy period (the length of coverage), the named insured (the person(s) covered by the policy), and the covered vehicles. The policy will also detail the limits of liability for each coverage type, specifying the maximum amount the insurance company will pay for covered losses. For instance, a 100/300/100 liability policy means the insurer will pay up to $100,000 for injuries to one person, $300,000 for injuries to multiple people in a single accident, and $100,000 for property damage. Understanding these limits is vital to ensuring you have adequate protection. Failure to comply with policy conditions, such as providing timely notice of an accident, could impact your claim.

Filing a Claim

The claims process typically begins by contacting your insurance company as soon as possible after an accident. You’ll need to provide detailed information about the accident, including the date, time, location, and involved parties. Police reports, witness statements, and photographic evidence are often helpful. The insurance company will then investigate the claim, which may involve contacting witnesses, reviewing police reports, and assessing the damage to vehicles. Following the investigation, the insurance company will determine liability and make a decision regarding payment of the claim. If the claim is denied, the policyholder has the right to appeal the decision. The specifics of the claims process, including required documentation and timelines, are typically Artikeld in the policy documents. Delays can occur due to factors like the complexity of the claim or disputes over liability.

Situations Where Different Coverages Apply

Different types of coverage address various accident scenarios. For example, liability coverage would apply if you cause an accident that injures another person or damages their property. Uninsured/underinsured motorist coverage protects you if you’re involved in an accident with a driver who lacks sufficient insurance or is uninsured. Collision coverage pays for damage to your vehicle regardless of fault, while comprehensive coverage covers damage from events like theft, fire, or hail. Personal injury protection (PIP) covers medical expenses and lost wages for you and your passengers, regardless of fault. For instance, if a deer runs into your car, comprehensive coverage would likely pay for the repairs. If you rear-end another car and are at fault, your liability coverage would cover the other driver’s damages, while your collision coverage would cover your car’s repairs. If you are hit by an uninsured driver, your uninsured/underinsured motorist coverage would apply.

Policy Exclusions and Limitations

| Exclusion/Limitation | Description | Example | Impact |

|---|---|---|---|

| Driving Under the Influence (DUI) | Coverage may be denied or significantly reduced if the accident involved DUI. | A driver causes an accident while intoxicated. | Claim denial or reduced payout. |

| Using a Vehicle Without Permission | Coverage may not apply if the driver was using the vehicle without the owner’s consent. | Someone borrows a car without the owner’s knowledge and causes an accident. | No coverage for damages. |

| Racing or Stunt Driving | Coverage is typically excluded for accidents occurring during illegal activities. | An accident occurs during an illegal street race. | Claim denial. |

| Wear and Tear | Damage caused by normal wear and tear is generally not covered. | A tire blows out due to normal wear and tear. | Repairs not covered. |

Resources for Affordable Auto Insurance in Illinois

Securing affordable auto insurance in Illinois can be challenging, especially for individuals and families with limited incomes. Fortunately, several resources and programs exist to assist in navigating the process and finding cost-effective coverage. This section will Artikel some key resources and programs available to help Illinois residents find affordable auto insurance.

State Resources and Organizations Offering Assistance

The Illinois Department of Insurance (IDOI) plays a crucial role in regulating the insurance market and protecting consumers. While they don’t directly provide financial assistance, the IDOI offers valuable resources to help you understand your rights and find suitable insurance options. They can provide information on insurance companies, compare rates, and address complaints regarding insurance practices. Additionally, various non-profit organizations across the state often offer free or low-cost insurance counseling services. These organizations can guide you through the process of finding affordable insurance, explaining policy details, and helping you compare different plans.

Programs for Low-Income Individuals

Several programs in Illinois aim to help low-income individuals obtain auto insurance. While a comprehensive state-sponsored program providing direct financial assistance for auto insurance premiums doesn’t exist, some community organizations and charities may offer limited assistance or subsidies in specific circumstances. It’s crucial to explore local resources and contact community action agencies or social service organizations in your area. They may be aware of local initiatives offering support for car insurance costs. These programs frequently have eligibility requirements based on income and household size.

Applying for Financial Assistance Programs

The application process for financial assistance varies significantly depending on the specific program. Generally, you’ll need to provide documentation demonstrating your income, household size, and the need for assistance. This often includes pay stubs, tax returns, and proof of residency. Some programs may require an interview to assess your eligibility. It’s recommended to thoroughly review the program guidelines and eligibility criteria before beginning the application process. Contacting the organization directly is crucial to obtain the most up-to-date application materials and understand specific requirements.

Relevant Websites and Contact Information

Finding the right resources requires knowing where to look. Here’s a starting point for your search:

- Illinois Department of Insurance (IDOI): Website: [Insert IDOI Website Address Here]; Phone: [Insert IDOI Phone Number Here]

- United Way of Illinois: Website: [Insert United Way of Illinois Website Address Here]; Phone: [Insert United Way of Illinois Phone Number Here] (Note: Contact your local United Way chapter for specific assistance programs.)

- Local Community Action Agencies: Contact your local government or social services department to find the contact information for your area’s Community Action Agency. These agencies often offer a range of assistance programs, including referrals for insurance help.

Illustrative Examples of Insurance Scenarios

Understanding the nuances of auto insurance in Illinois can be challenging. These examples illustrate how different coverage levels and driving habits impact your premiums and protection.

Minimum Coverage versus Comprehensive Coverage Cost Difference

Let’s consider two drivers, both 30 years old with clean driving records living in a suburban area of Chicago. Driver A chooses the state-mandated minimum liability coverage, while Driver B opts for comprehensive coverage, including collision and uninsured/underinsured motorist protection. Driver A’s annual premium might be around $500, while Driver B’s premium could be closer to $1200. This significant difference reflects the broader protection offered by comprehensive coverage. The higher cost reflects the greater financial risk the insurance company assumes in covering a wider range of potential damages.

Hypothetical Accident and Insurance Coverage Application

Imagine a scenario where Driver A (minimum coverage) is involved in an accident. Their car, valued at $10,000, is totaled due to a collision with another vehicle. Driver A is at fault. Their minimum liability coverage might only cover the other driver’s vehicle damage, leaving Driver A responsible for the cost of their own vehicle repairs or replacement. Conversely, if Driver B (comprehensive coverage) were involved in the same accident, their comprehensive coverage would cover the repair or replacement of their own vehicle, regardless of fault. Their collision coverage would also likely cover any damage to their car, even if they were at fault. Uninsured/underinsured motorist protection could also protect them if the at-fault driver had inadequate insurance.

Impact of a Poor Driving Record on Insurance Premiums

Consider two drivers, both with similar vehicles and coverage levels. Driver C has a clean driving record, while Driver D has received three speeding tickets and one at-fault accident in the past three years. Driver C’s annual premium might be $800, while Driver D’s premium could easily exceed $1500, even with the same coverage. Insurance companies consider driving history a significant risk factor, and multiple incidents lead to higher premiums to compensate for the increased likelihood of future claims. This illustrates the importance of safe driving habits in maintaining affordable insurance costs.

Savings from Bundling Home and Auto Insurance

Let’s say Driver E has both a home and an auto insurance policy with separate companies. Their annual auto premium is $1000, and their home premium is $1200. If Driver E bundled their home and auto insurance with a single insurer, they might receive a discount of 10-15%, resulting in a combined annual premium of approximately $2000 – $2070. This demonstrates the significant cost savings that can be achieved through bundling policies, often due to the insurer’s reduced administrative costs and the increased loyalty of bundled customers.

Closing Notes

Finding affordable auto insurance in Illinois requires careful planning and comparison shopping. By understanding the factors influencing your premiums, utilizing online comparison tools, and exploring available discounts, you can significantly reduce your insurance costs without compromising necessary coverage. Remember to review your policy regularly and adjust your coverage as needed to ensure you’re adequately protected while maintaining affordability.

Question & Answer Hub

What is SR-22 insurance and do I need it?

SR-22 insurance is proof of financial responsibility required by the state after certain driving offenses. You only need it if mandated by the Illinois Secretary of State.

Can I pay my insurance premiums monthly?

Most insurance companies offer monthly payment plans, but this may involve additional fees. Check with your chosen provider for details.

How often can I expect my insurance rates to change?

Rates can change annually or even more frequently, depending on factors like your driving record and claims history. Regularly review your policy and shop around for better rates.

What happens if I get into an accident and don’t have enough coverage?

Insufficient coverage can leave you personally liable for costs exceeding your policy limits. This could lead to significant financial burdens.