Securing your business’s future requires a robust insurance strategy. AAA Business Insurance offers a range of comprehensive coverage options designed to protect against various risks, from property damage to liability claims. This guide delves into the key features, benefits, and considerations of AAA Business Insurance, empowering you to make informed decisions about protecting your valuable assets and mitigating potential financial setbacks.

We will explore the different types of coverage available, factors influencing premium costs, the claims process, and a comparison with competitor offerings. Understanding these aspects will allow you to choose a policy that best aligns with your business’s specific needs and risk profile, ensuring peace of mind and financial stability.

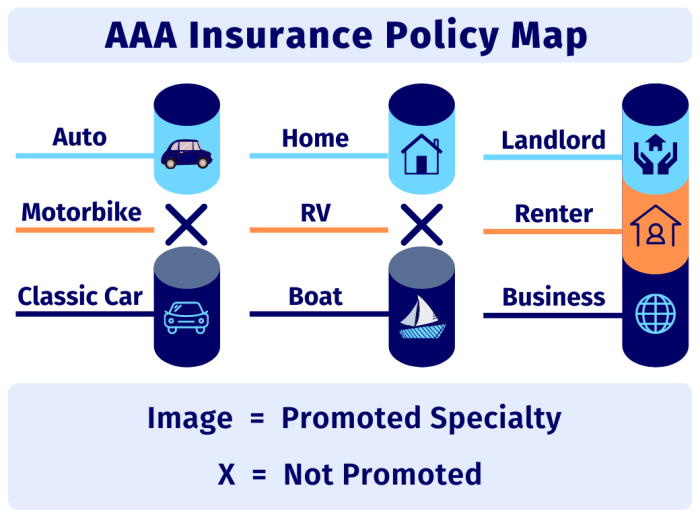

Defining AAA Business Insurance

AAA Business Insurance, often offered as part of a broader suite of services by AAA (American Automobile Association) affiliates, provides a range of coverage options designed to protect small to medium-sized businesses from various financial risks. While the specific policies and coverage vary by location and provider, the core aim remains consistent: to offer comprehensive protection at a competitive price point, leveraging the established reputation and network of the AAA brand.

AAA Business Insurance policies typically bundle several key components into a single package, offering convenience and cost-effectiveness. These components usually include property insurance (covering buildings and equipment), liability insurance (protecting against lawsuits), and potentially business interruption insurance (compensating for lost income due to unforeseen events). The specific inclusions depend heavily on the individual policy and the nature of the business.

Types of Businesses Covered by AAA Business Insurance

AAA Business Insurance is generally designed for smaller businesses, although the specific size limits may vary depending on the insurer and location. Commonly covered business types include retail stores, restaurants, offices, and small manufacturing facilities. Larger enterprises often require more specialized and comprehensive insurance solutions that may not be fully addressed within a standard AAA Business Insurance package. Businesses operating in high-risk industries might find their needs better served by insurers specializing in those sectors.

Common Risks Addressed by AAA Business Insurance

AAA Business Insurance addresses several common risks faced by small businesses. Property damage from fire, theft, or natural disasters is a primary concern, and coverage typically extends to the business premises, equipment, and inventory. Liability insurance is crucial for protecting against lawsuits stemming from accidents or injuries on business property or related to the business’s operations. Business interruption insurance helps businesses recover lost income if operations are temporarily suspended due to a covered event, such as a fire or a natural disaster. For example, a restaurant facing a fire might be covered for lost revenue while repairs are undertaken.

Comparison of AAA Business Insurance with Other Types of Business Insurance

Compared to other business insurance providers, AAA Business Insurance often emphasizes convenience and potentially competitive pricing, particularly for members. However, the breadth and depth of coverage might be more limited than what larger, specialized insurers offer. For instance, a national insurance company might provide more nuanced coverage options for specific industries or offer higher coverage limits. The choice between AAA Business Insurance and other providers depends on the individual business’s specific needs, risk profile, and budget. A small bakery might find AAA sufficient, while a large construction company might require a more specialized and extensive policy from a different provider.

Coverage Options within AAA Business Insurance

AAA Business Insurance offers a range of coverage options designed to protect various aspects of your business. Understanding these options and their implications is crucial for securing the right level of protection tailored to your specific needs and risk profile. The choice of coverage will depend heavily on the size, type, and location of your business, as well as the potential liabilities you face.

General Liability Insurance

General liability insurance protects your business from financial losses due to third-party claims of bodily injury or property damage caused by your business operations. This is a fundamental coverage for most businesses, regardless of size. For example, if a customer slips and falls on your premises, general liability insurance would cover the resulting medical expenses and potential legal fees. This coverage typically excludes intentional acts and damage to your own property. The policy limits and deductibles vary depending on the chosen plan.

Commercial Auto Insurance

If your business uses vehicles for deliveries, transportation of goods, or employee commuting, commercial auto insurance is essential. This coverage protects you from financial losses resulting from accidents involving your company vehicles. It covers damages to other vehicles and property, medical expenses for injured parties, and legal costs associated with accidents. The level of coverage (e.g., liability, collision, comprehensive) is customizable, influencing both premium and deductible amounts. For instance, a business using multiple delivery vans would require a higher level of coverage than a business with a single company car.

Workers’ Compensation Insurance

Workers’ compensation insurance protects your employees in the event of work-related injuries or illnesses. It covers medical expenses, lost wages, and rehabilitation costs for injured employees. It also protects your business from potential lawsuits filed by injured workers. This is a mandatory coverage in many states and is vital for protecting your employees and your business’s financial stability. Failing to carry adequate workers’ compensation insurance could result in significant financial penalties.

Professional Liability Insurance (Errors and Omissions Insurance)

Professional liability insurance, also known as Errors and Omissions (E&O) insurance, protects professionals like consultants, designers, and lawyers from claims of negligence or mistakes in their professional services. This coverage is crucial for businesses that provide professional services, as it safeguards against costly lawsuits resulting from errors or omissions in their work. For example, an architect who makes a design error that leads to structural damage could be covered by E&O insurance.

Commercial Property Insurance

Commercial property insurance protects your business property from damage or loss due to various perils such as fire, theft, vandalism, and natural disasters. This coverage can include the building itself, its contents, and any equipment. It provides financial protection for repairs, replacements, and business interruption expenses. A restaurant, for example, would benefit greatly from commercial property insurance to protect against fire damage or theft of equipment.

Table Comparing Coverage Options

| Coverage Option | Premium Range (Annual) | Deductible Range | Benefits |

|---|---|---|---|

| General Liability | $500 – $5,000+ | $500 – $5,000+ | Protects against third-party claims of bodily injury or property damage. |

| Commercial Auto | $1,000 – $10,000+ | $250 – $1,000+ | Covers accidents involving company vehicles. |

| Workers’ Compensation | Varies greatly by state and payroll | Varies by state and policy | Covers work-related injuries and illnesses for employees. |

| Professional Liability | $500 – $5,000+ | $250 – $1,000+ | Protects against claims of negligence or mistakes in professional services. |

| Commercial Property | $500 – $10,000+ | $500 – $5,000+ | Protects against damage or loss to business property. |

Factors Affecting AAA Business Insurance Premiums

Understanding the factors that influence your AAA business insurance premiums is crucial for effective budget planning and risk management. Several key elements contribute to the final cost, and a thorough understanding of these can help you secure the best possible coverage at a competitive price. This section will detail those key factors and offer strategies for potentially reducing your premium costs.

Several interconnected factors determine the cost of your AAA business insurance premiums. These factors are carefully assessed by insurers to accurately reflect the level of risk associated with your specific business. A higher perceived risk translates to higher premiums, while effective risk mitigation strategies can lead to lower costs.

Business Size and Revenue

Business size directly impacts insurance premiums. Larger businesses with higher revenues generally face higher premiums due to increased potential liabilities and claims. For instance, a large manufacturing company with numerous employees and extensive operations will naturally present a higher risk profile than a small home-based business. Insurers consider factors like employee count, annual revenue, and the complexity of operations when calculating premiums. A larger workforce, for example, increases the likelihood of workplace accidents and associated claims. Similarly, a business with high revenue is often associated with a higher potential for lawsuits or significant property damage.

Business Location

Geographic location plays a significant role in determining insurance premiums. Businesses located in high-risk areas, such as those prone to natural disasters (hurricanes, earthquakes, floods), or areas with high crime rates, will typically face higher premiums. For example, a business situated in a coastal region vulnerable to hurricanes will likely pay more for property insurance than a similar business located inland. Similarly, a retail store in a high-crime area might face higher premiums for theft and vandalism coverage. Insurers use sophisticated risk assessment models that incorporate location-specific data to accurately price insurance policies.

Industry Type

The industry in which your business operates is a primary factor influencing premium costs. High-risk industries, such as construction or manufacturing, generally have higher premiums due to the increased likelihood of accidents and injuries. Conversely, businesses in lower-risk industries might enjoy lower premiums. For example, a software company is likely to have lower insurance premiums compared to a construction company, reflecting the inherent differences in risk profiles. Insurers maintain detailed industry-specific risk profiles, incorporating data on past claims and industry-specific hazards.

Risk Mitigation Strategies to Lower Premiums

Implementing effective risk mitigation strategies can significantly reduce your insurance premiums. These strategies demonstrate to insurers your commitment to safety and risk management, leading to a lower perceived risk and consequently, lower premiums.

- Improved Safety Measures: Implementing robust safety protocols in the workplace, such as providing safety training to employees and investing in safety equipment, can significantly reduce the likelihood of workplace accidents, leading to lower workers’ compensation premiums.

- Security Systems: Installing advanced security systems, including alarm systems, security cameras, and access control systems, can help reduce the risk of theft and vandalism, potentially lowering property insurance premiums.

- Regular Maintenance: Regular maintenance of equipment and facilities helps prevent accidents and reduces the risk of property damage, potentially leading to lower premiums for property and liability insurance.

- Risk Assessments: Conducting regular risk assessments helps identify potential hazards and allows you to implement preventative measures, demonstrating proactive risk management to insurers.

Common Misconceptions Regarding AAA Business Insurance Costs

Several misconceptions surround the cost of AAA business insurance. Understanding these misconceptions can help you make informed decisions about your coverage.

- Higher Premiums Always Mean Better Coverage: This is not necessarily true. While higher premiums often indicate broader coverage, it’s essential to carefully compare policies and coverage details to ensure you’re getting the best value for your money.

- Small Businesses Don’t Need Comprehensive Insurance: Even small businesses face significant risks and can benefit from comprehensive insurance protection. Underestimating your risk exposure can have severe financial consequences.

- Insurance is a Fixed Cost: Insurance premiums are not static; they can be influenced by several factors, including risk mitigation strategies and changes in your business operations.

- Shopping Around is Unnecessary: Comparing quotes from different insurers is crucial to securing the best possible rates and coverage. Different insurers have varying risk assessments and pricing structures.

Claim Process and Customer Support

Navigating the claims process after an unforeseen incident can be stressful for any business owner. AAA Business Insurance aims to simplify this experience by providing a straightforward and supportive process, complemented by readily available customer service. Understanding the steps involved and the resources available will help ensure a smoother claim resolution.

The typical claim process for AAA Business Insurance begins with the immediate reporting of the incident. This is followed by a thorough investigation and assessment of the damages or losses incurred. Once the claim is validated, the insurer will process the payment according to the policy’s terms and conditions. Throughout this process, policyholders have access to dedicated customer support channels to address any questions or concerns.

Claim Filing Best Practices

Efficient and effective claim filing significantly reduces processing time and ensures a timely resolution. Key steps include promptly reporting the incident, gathering all necessary documentation (such as police reports, repair estimates, and invoices), and accurately completing the claim form. Providing comprehensive and accurate information from the outset prevents delays and ensures a smoother claims experience. Maintaining detailed records of your business’s assets and operations can also prove invaluable during the claims process. For example, maintaining photographic evidence of inventory before a theft would greatly aid in the valuation of lost goods.

AAA Business Insurance Customer Support Options

AAA provides multiple avenues for policyholders to access customer support. These include a dedicated phone line staffed by knowledgeable representatives available during extended business hours, a user-friendly online portal for claim tracking and policy management, and email support for less urgent inquiries. Policyholders can also schedule in-person meetings with local AAA representatives for personalized assistance. The availability of these diverse support channels ensures that assistance is accessible regardless of individual preferences or time constraints. For instance, a policyholder facing an immediate emergency might prefer a phone call, while someone needing to track their claim’s progress might opt for the online portal.

Claim Filing Flowchart

Imagine a flowchart visually representing the claim process. It would begin with “Incident Occurs.” This would branch to “Report Incident to AAA (Phone, Online, or In-Person).” The next step would be “AAA Investigates Claim.” This leads to two possible outcomes: “Claim Approved” or “Claim Denied.” If approved, the flow continues to “Payment Processed.” If denied, the process branches to “Review Denial Reasons and Appeal (If Applicable).” Regardless of approval or denial, the flowchart concludes with “Claim Resolution.” This visual representation clearly Artikels the steps involved and helps policyholders understand the process’s flow.

Comparing AAA Business Insurance with Competitors

Choosing the right business insurance is crucial for protecting your assets and ensuring your business’s continued success. This section compares AAA Business Insurance with other major providers, highlighting its strengths, weaknesses, and key differentiators to help you make an informed decision. We’ll examine various aspects, including coverage options, pricing, and customer service.

AAA Business Insurance offers a competitive suite of products designed to meet the needs of various businesses. However, a direct comparison with other major players in the market provides a more comprehensive understanding of its position and value proposition.

AAA Business Insurance Strengths and Weaknesses Compared to Competitors

AAA Business Insurance benefits from its established reputation and extensive network. This translates to potentially quicker claims processing and broader access to resources. However, depending on the specific business needs and location, premiums might be higher compared to some competitors who offer more niche or specialized coverage at lower costs. Furthermore, the breadth of coverage offered by AAA might not match the hyper-specialized offerings of some competitors focusing on specific industries. The competitive landscape is dynamic, and a thorough review of individual policy details is always recommended.

Key Differentiators of AAA Business Insurance

AAA’s key differentiator often lies in its bundled services. Many AAA members already benefit from roadside assistance and other services, and adding business insurance might create a seamless and convenient package. This bundled approach can simplify the management of various insurance needs for business owners. Another potential differentiator is the strong brand recognition and customer trust associated with the AAA name, which can be particularly important for building confidence in a provider. However, it’s crucial to compare the actual policy details and coverage rather than relying solely on brand reputation.

Comparison Table of Business Insurance Providers

This table provides a high-level comparison. Actual pricing and coverage will vary based on individual business needs and risk profiles. Always consult directly with insurance providers for accurate quotes and detailed policy information.

| Insurance Provider | General Liability Coverage | Property Coverage | Professional Liability (Errors & Omissions) | Approximate Premium Range (Annual) |

|---|---|---|---|---|

| AAA Business Insurance | Yes, various options available | Yes, building and contents | Available as an add-on | $500 – $5000+ |

| Competitor A (e.g., The Hartford) | Yes, customizable options | Yes, various coverage levels | Yes, included or add-on | $400 – $4000+ |

| Competitor B (e.g., Nationwide) | Yes, various packages | Yes, building and contents | Available as an add-on | $600 – $6000+ |

| Competitor C (e.g., State Farm) | Yes, standard and enhanced options | Yes, comprehensive coverage | Available as an add-on | $550 – $5500+ |

Illustrative Scenarios & Case Studies

AAA Business Insurance offers comprehensive protection, and understanding its value requires exploring real-world applications. The following scenarios highlight how our various coverage options have benefited businesses, showcasing the importance of adequate insurance and the effectiveness of our claim process.

Successful Claim for Property Damage After a Storm

Imagine a small bakery, “Sweet Surrender,” located in a coastal town. A severe storm causes significant damage to their storefront, including broken windows and water damage to the interior. Sweet Surrender had comprehensive property damage coverage with AAA Business Insurance. Their claim was processed efficiently; an adjuster visited the site quickly, assessed the damage, and approved the necessary repairs. The insurance covered the cost of repairs, including replacing windows, fixing water damage, and temporarily relocating their operations while repairs were underway. This allowed Sweet Surrender to minimize business interruption and quickly resume operations, preventing significant financial losses. The entire claim process took less than three weeks, demonstrating AAA’s commitment to swift and supportive customer service.

Business Interruption Coverage After a Cyberattack

“Tech Solutions,” a rapidly growing IT firm, experienced a debilitating cyberattack that crippled their systems and resulted in lost data and downtime. Tech Solutions had purchased AAA’s business interruption insurance, which covered lost revenue and expenses incurred during the recovery period. The policy reimbursed them for lost profits, the cost of hiring cybersecurity experts to restore their systems, and the expense of notifying affected clients. The policy also included funds to help Tech Solutions implement enhanced cybersecurity measures to prevent future attacks. This prevented a potentially catastrophic financial blow, allowing Tech Solutions to recover and continue operations without facing crippling debt.

Liability Claim Following a Customer Injury

“Active Adventures,” an outdoor recreation company, faced a liability claim when a customer was injured during a guided hiking tour. The customer suffered a broken leg and sued Active Adventures for negligence. AAA Business Insurance’s general liability coverage protected Active Adventures from significant financial losses. AAA’s legal team defended Active Adventures throughout the litigation process, negotiating a settlement that was far less than the potential damages. This case highlights the importance of liability coverage, even for businesses that strive to maintain high safety standards.

Impact of Inadequate Coverage: A Hypothetical Example

Consider a local restaurant, “The Cozy Corner,” that opted for minimal liability insurance. A customer suffered severe food poisoning after dining at the restaurant. The resulting lawsuit far exceeded the limits of their insurance policy, forcing The Cozy Corner to cover the remaining costs, ultimately leading to the restaurant’s closure due to insurmountable debt. This scenario emphasizes the potential financial devastation that can result from insufficient insurance coverage, highlighting the importance of comprehensive protection.

Final Summary

Choosing the right business insurance is a crucial step in safeguarding your business’s financial health and long-term viability. AAA Business Insurance presents a comprehensive solution, but careful consideration of your individual needs and a thorough comparison with other providers are essential. By understanding the coverage options, premium factors, and claims process, you can confidently select a policy that offers the appropriate level of protection and provides the reassurance necessary to focus on growing your business.

Quick FAQs

What types of businesses are eligible for AAA Business Insurance?

AAA Business Insurance typically covers a wide range of businesses, from small startups to established enterprises across various industries. However, specific eligibility criteria may vary depending on the type of business and risk profile.

What is the typical response time for a claim?

AAA aims to process claims efficiently. The exact timeframe depends on the complexity of the claim and the required documentation. Contacting their customer support directly will provide the most accurate estimate.

Can I customize my AAA Business Insurance policy?

Yes, AAA Business Insurance offers various coverage options and customizable packages to tailor the policy to your specific business needs and risk assessment.

How often are premiums reviewed?

Premium reviews are typically conducted annually, but this may vary depending on the policy terms and any changes in your business operations or risk profile.